The World’s Largest Ponzi Scheme

By: David D. Schein

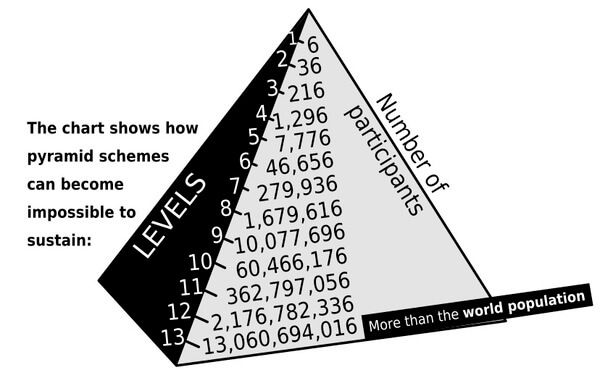

“Ponzi Scheme” is a term that was coined about 100 years ago. It was named after an Italian immigrant, Charles Ponzi, who realized he could get investors by promising large returns for undefined, high-yield investments. His endeavor needed to make just enough money to keep attracting new investors, whose money, after Ponzi’s cut, was used to pay some of the earlier investors. In our modern day, Bernie Madoff’s Ponzi scheme resulted in losses in the billions of dollars when the stock market tanked during the Great Recession.

Selling the Deal

Americans are just beginning to see the tip of the iceberg of their own trillion-dollar Ponzi scheme, Social Security (“SSA”). Signed into law in 1935 by FDR during the heart of the Great Depression, workers were told that Social Security was intended to provide a safety net parallel to retirement systems that existed in Europe. The retirement age was set at 65. Americans were required to pay into the fund through payroll deductions their employers collected. Most Americans were “covered” by the system, and it was later expanded to cover household workers and others who were excluded initially. The system is structured to be a regressive income tax covering most workers’ wages up to $160,200 per year, with no limit on the parallel Medicare withholding.

When FDR was garnering praise for helping the working class, the average life expectancy in the United States was only 60.7 years. So, while most workers would pay into the system, few would live long enough to collect benefits.

In contrast, by 2020, the average American life expectancy had surged to 78.81 years. This is just one of the problems with the SSA’s structure that has brought America to the current financial cliff. Obviously, if most of the alleged beneficiaries would not live long enough to collect, it was a near-perfect scheme for its operator. The “baby boomer” generation, by expanding the system’s benefits and living longer, is tanking the system.

Private Sector Comparison

In the mid-1960s, Studebaker, a manufacturer that progressed from covered wagons to automobiles, filed for bankruptcy. It turned out that Studebaker had borrowed from its employee pension funds as its finances were declining, making the company IOUs in the pension fund worthless and the fund significantly underfunded. The unionized workers’ outcry reached Congress. Congress rushed a law requiring employer pension funds to be actuarially determined so that the promised pension benefits would be there at retirement. It also required that these monies be set aside in special accounts exclusively for the workers’ benefit. “Rushed” might be a bit of an exaggeration. It wasn’t until 1974, a decade after Studebaker’s bankruptcy, that Congress passed the Employee Retirement and Income Security Act (“ERISA”), a law that basically said an employer “shall not steal from its employee pension funds.”

The Financial Cliff

Under ERISA, Congress mandated that, if a private employer promised a pension, the benefit had to be there when the employee qualified for the payments. However, Congress did not designate the same protection for the largest employee benefit program in American history. Due initially to the limited American life span in the early days of the program, SSA ran at a surplus. Post-WWII, the baby boomers surged into the workforce, and SSA collected more money than needed to pay current benefits.

Then, around 2011, the first boomers hit 65. There is no magic to this formula. Just a decade later, the Social Security Trust Fund is already a patient on life support, and the end is around the corner in 2033. Available to all is the Congressional Budget Office’s “2022 Long-Term Projections for the Social Security.” The shortfall is in the trillions of dollars beyond that date with no turnaround in place. In fact, attentive Americans of all ages should have noted that, during the current National Debt Limit debate, if the government did not raise the limit by June 5, SSA payments would have been stopped.

There was more than a big demand, though, to account for the shortfall when the Boomers aged into the SSA program. The surplus funds were used to buy US Government securities, which until recently, have been at historically low rates since the Great Recession. So, just as Studebaker did, the United States used the SSA funds to finance itself.

Prior fixes in 1983 included taxing SSA benefits at 50% for persons earning at least $25,000 per year and gradually increasing the normal retirement age from 65 to 67. A decade later, SSA benefits were taxed at 85% after earning $34,000 per year. The maximum benefit for someone retiring in 2023 at age 70 is currently capped at $4,555 per month.

None of this explains a near-total lack of attention from Congress. In fact, the SSA increased the monthly benefit by 8.7% effective January 2023. The SSA was able to do this without congressional approval. This hardly indicates a recognition of the cliff ahead.

Action Plan

While cutting benefits and/or increasing the SSA withholding would have some significant blowback on the politicians who implement these measures, it is hard to imagine other functional fixes. Recently, it has been suggested that normal retirement age be increased to 70 from 67.

A more creative solution was proposed by a commission established by President George W. Bush in 2001. The commission recommended that younger workers be allowed to direct some of their SSA payments into a conservative mix of stocks and bonds. However, even during Bush’s most popular period, that did not pass. Following his reelection in 2004, he tried again, but his political support evaporated under the negative publicity following the bungled response to Hurricane Katrina. Early in his administration, President Barack Obama also raised the issue of preserving SSA, but that went nowhere.

The importance of SSA retirement benefits cannot be overemphasized. A recent report by the SSA indicated that 90% of people 65 and older were receiving SSA benefits, representing about 30% of the income for this age group. There is no solution to this problem without pain. One thing is certain: The longer Congress waits to fix it, the more painful the solution.

Wrap

Typical of all Ponzi schemes, the operator never really intended to pay the majority of those who paid into the system. Many early SSA recipients, in the years from 1940-2020, were able to benefit from payments by later contributors. Now that the addition of new workers has faded relative to those attempting to draw from the system, the later contributors face getting far less than they should receive, assuming SSA survives at all.

••••

This article (The World’s Largest Ponzi Scheme) is republished here on TLB under “Fair Use” (see the TLB disclaimer below article) with attribution to the author David D. Schein and americanthinker.com.

TLB recommends that you visit the American Thinker for more great articles and info.

More Articles by: David D. Schein

Image Credit: Photo (cropped) in Featured Image (top) – “Social Security Card – Illustration” by DonkeyHotey is licensed under CC BY 2.0. and In-Article image: The SEC’s illustration of a Ponzi scheme. Public domain.

••••

Related Article:

‘Bidenomics’ In Layman’s Terms Is Foreign Corruption & Government Control

••••

Checkout TLBTalk.com:

Click Here to Visit the TLBTalk.com Site

••••

Welcome to the TLB Project Neighborhood

TLBTalk – Republic Broadcasting Network – The Liberty Beacon – The Butcher Shop

••••

••••

Stay tuned to …

••••

The Liberty Beacon Project is now expanding at a near exponential rate, and for this we are grateful and excited! But we must also be practical. For 7 years we have not asked for any donations, and have built this project with our own funds as we grew. We are now experiencing ever increasing growing pains due to the large number of websites and projects we represent. So we have just installed donation buttons on our websites and ask that you consider this when you visit them. Nothing is too small. We thank you for all your support and your considerations … (TLB)

••••

Comment Policy: As a privately owned web site, we reserve the right to remove comments that contain spam, advertising, vulgarity, threats of violence, racism, or personal/abusive attacks on other users. This also applies to trolling, the use of more than one alias, or just intentional mischief. Enforcement of this policy is at the discretion of this websites administrators. Repeat offenders may be blocked or permanently banned without prior warning.

••••

Disclaimer: TLB websites contain copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to our readers under the provisions of “fair use” in an effort to advance a better understanding of political, health, economic and social issues. The material on this site is distributed without profit to those who have expressed a prior interest in receiving it for research and educational purposes. If you wish to use copyrighted material for purposes other than “fair use” you must request permission from the copyright owner.

••••

Disclaimer: The information and opinions shared are for informational purposes only including, but not limited to, text, graphics, images and other material are not intended as medical advice or instruction. Nothing mentioned is intended to be a substitute for professional medical advice, diagnosis or treatment.

Leave a Reply