Trump will never…

via Nordea

Written by Martin Enlund and Andreas Steno Larsen

Trump seems to be winning the trade war from an equity market point-of-view. At the same time the implied probability of Trump leaving office prematurely has plummeted. Yet many keep saying that “Trump will never..”, but we think he means business.

Trump will never

The market has been awash with trade war fears, and these worries appear to have been picking up recently, as evidenced by commentary from multinational companies as well as from ECB and Fed officials (e.g. Bullard, Bostic). The trade war noise is, however, becoming a negative risk for global macro as it is easy for companies to delay investment plans when uncertainty picks up. This is something that could expedite our grinding slowdown scenario and, if worse comes to worse, lead to a more pronounced recession risk.

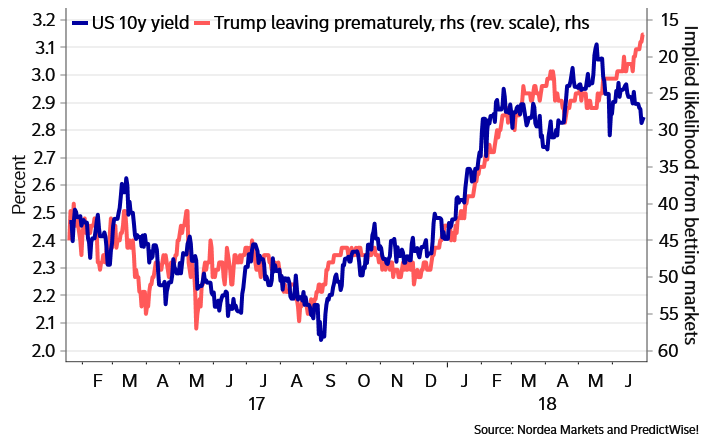

Chart 1: Trump leaving prematurely? Fuhgeddaboudit

Alas, these trade fears have yet to affect his popularity, which has been on a rising trend. Indeed, on a recent Gallup poll, he had the highest approval rate since his inauguration. Maybe the market is still underestimating him, as it has had a tendency to do for some years. For instance, Donald Trump spoke about slapping 25% tariffs on China already in early 2011, and here we are. He does seem to mean business.

Table 1: Trump will never

And while many expect that the eventual Mueller report (“Russiagate”) to doom the White House any day now, that has been a losing proposition so far. The likelihood that President Trump will be forced out of the White House prematurely has actually been plummeting. It does seem as if the market will remain stuck with the guy.

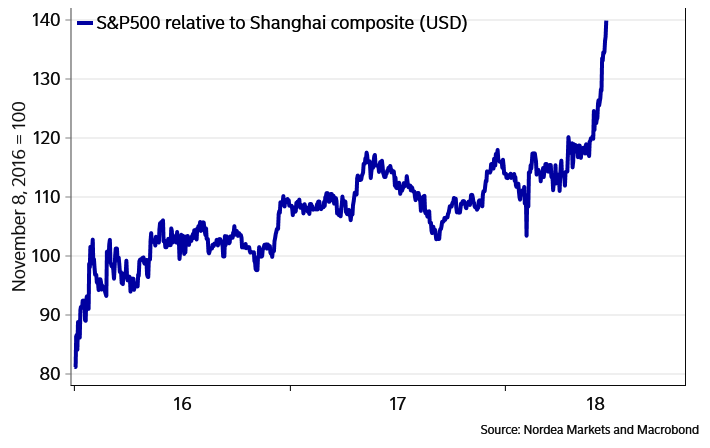

Chart 2: US is winning its trade war against China, from an equity market point-of-view

From the perspective of the equity market, it seems as if the US is indeed winning the trade war, at least vs China. The S&P500 index holds up quite well, while the Shanghai Composite index has tanked 15% year-to-date in CNY. The recent swoon in Chinese equities suggests downside risks to activity, and indicators such as Chinese PMI manufacturing. If the authorities try to cushion this blow via allowing a weaker CNY, well, who can be surprised?

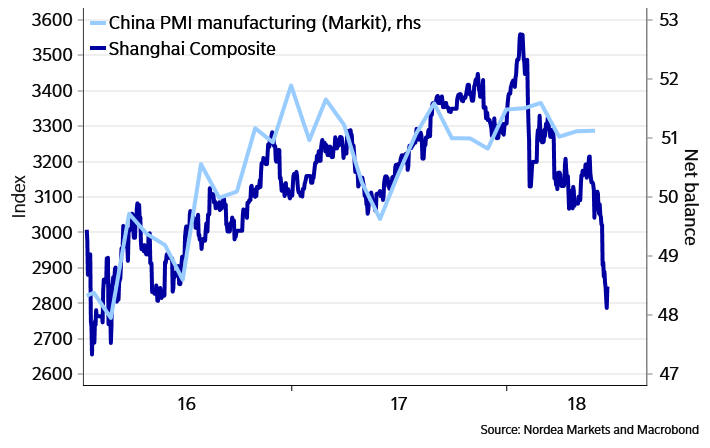

Chart 3: Chinese equities indicate downside risks to PMI

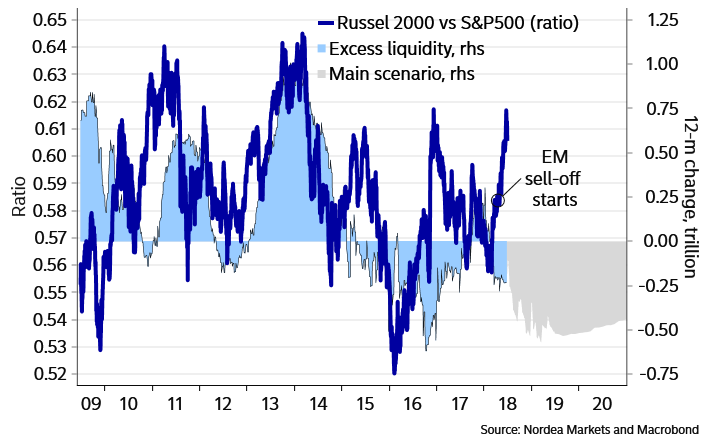

Interestingly, it might be that the money which has left EM en masse in recent months has entered US small caps which have outperformed. FAANGs, BATs, small caps and momentum strategies have all performed well recently. Alas, we do not expect small-caps to provide a safe haven in the macro climate which will gradually unfold in H2, 2018.

Chart 4: Has EM outflows led to inflows to small caps?

Is the EU swerving?

Only a few days ago, EU’s trade commissioner Malmström insisted EU had no plans to talk with the US about trade, at least as long as the US’ tariffs were in place. But suddenly, after the save-Merkel EU summit, Juncker has been tasked to go to Washington later in July “to talk trade”.

We have earlier compared the trade situation to a chicken race between e.g. EU and the US. In a classical example of a chicken race “two drivers drive towards each other on a collision course: one must swerve, or both may die in the crash, but if one driver swerves and the other does not, the one who swerved will be called a “chicken” (i.e. losing). Both the EU and the US would naturally be less well-off economically in a full-scale trade war, but if the US can extract some concessions from the EU (getting EU to swerve) it would be a relative winner. Now it looks as if the EU may be swerving. This may be good news for global trade, as it could de-escalate the situation.

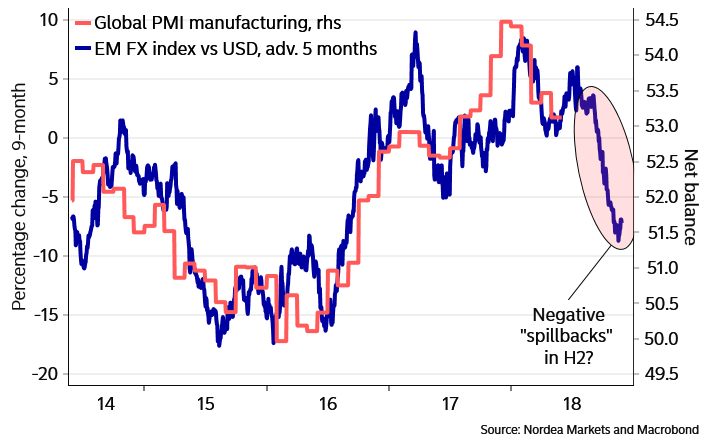

Chart 5: When will EM worries start to show up in global PMI?

Expect global PMI to weaken further later this year

We don’t sound the all clear in any way however. The Fed is letting its balance sheet shrink at a quicker and quicker pace, with a maximum shrinkage of USD50bn/month reached in Q4, 2018 (of which 30bn can be Treasury bonds and notes). This has process has contributed to EM weakness this year, and may undermine EM further in H2. We moreover think the recent tightening of global financial conditions, especially in emerging markets, will bring about plenty of negative spillovers on global macro.

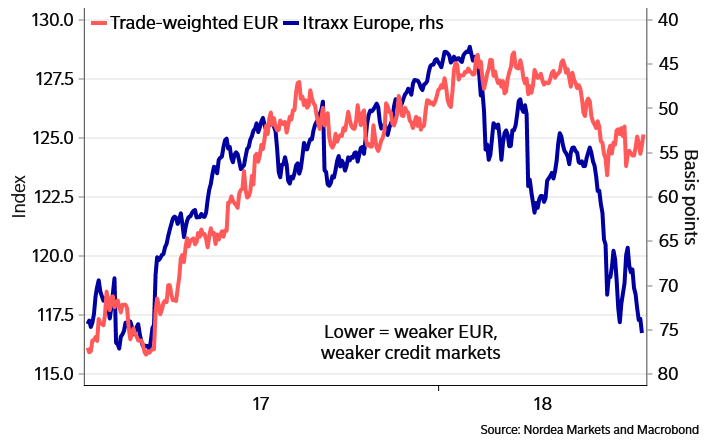

You also have to wonder what’s going in the Euro-area, where the recent spread widening and underperformance of certain sectors indicate further downside to the EUR. In the bigger picture, we add the widening of Itraxx indices to our list of canaries in the coal mine. The popping of the crypto currency bubble, liquidity problems in China, the collapse of inverse volatility products, EM commotion and Italian and Spanish bond market turmoil are examples of what you might expect to see if global growth is slowing, the cost of capital, especially in the US, is rising, and global central banks offer less liquidity support. Expect more of the same.

Chart 6: Itraxx indices indicate further EUR weakness

*********

(TLB) published this article by Martin Enlund and Andreas Steno Larsen from Nordea, a financial resource for your consideration.

••••

The Liberty Beacon Project is now expanding at a near exponential rate, and for this we are grateful and excited! But we must also be practical. For 7 years we have not asked for any donations, and have built this project with our own funds as we grew. We are now experiencing ever increasing growing pains due to the large number of websites and projects we represent. So we have just installed donation buttons on our main websites and ask that you consider this when you visit them. Nothing is too small. We thank you for all your support and your considerations … TLB

••••

Leave a Reply