by Lance Roberts

What a change a couple of weeks can make. As my colleague, Michael Lebowitz, wrote this past week:

“Following Donald Trump’s surprise victory and the violent market reactions, many investors are left scratching their heads. As shown above, the consensus narrative warned that a Trump victory would spell doom for the markets. Days later, the narrative flipped and Trump’s economic policies, all of which were known prior to the election, are deemed beneficial for share prices.”

The question which remains, however, is whether tax reform and infrastructure spending will have the impact the markets are currently betting on?

As I penned in yesterday’s missive:

“The problem for Trump is that we no longer reside in the 80’s where a large group of ‘baby boomers’ were entering the workforce and driving a massive wave of innovation and productivity changes. Today, we are on the wrong side of the demographic trends combined with falling productivity and labor force growth.”

“In any event, the horses may already be out of the barn. Only 8.5% of payroll employment is now attributable to manufacturing, down from 10.3% 10 years ago, 14.3% 20 years ago, and 17.5% 30 years ago. Bringing factory jobs back to the US may bring them back to automated factories loaded with robots. Even Chinese factories are using more robots.”

And from Harvard Business Review:

“Slow productivity growth is the main cause of slow economic growth, and slow economic growth makes it all but impossible for everyone’s boat to rise. No wonder angry citizens want dramatic change. But while voters may see the problem in a political establishment that is out of touch, the populist politicians who are challenging that establishment are unlikely to fare better.

In the short term, they may be able to medicate the economy with a big tax cut or a dose of deficit spending. When the effects of that treatment wear off, though, the effects of slow productivity growth will linger.”

But beyond the productivity problem is simply debt.

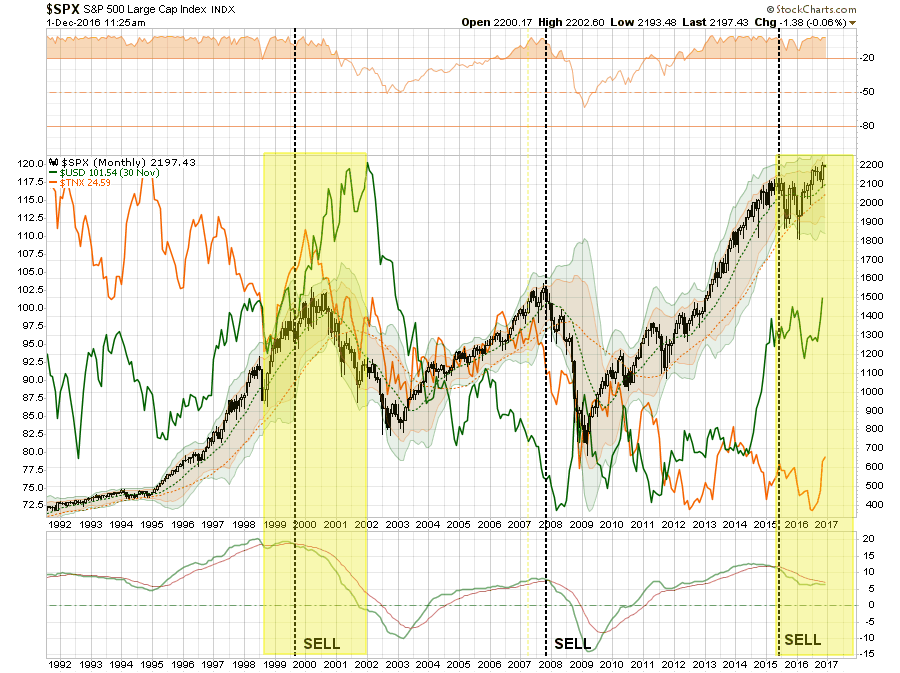

While Trumponomics has fostered a furious rally in asset prices, the impacts of rising interest rates, inflation, and a surging dollar may provide headwinds of the wrong type. In fact, the current combination of events is similar to what we saw previously – in 1999. (yellow highlights)

Also, notice there have only been three sell signals since 1999 as well which have coincided with major market peaks. If you look closely there is a high degree of similarity in the markets actions between today and the “exuberance” in 1999.

While I am not suggesting the market is about to “crash” in a fiery mass, I am suggesting the “ebullience” of the markets over the last 8-years has likely priced in any real net effects of fiscal policy changes at this point.

In other words, changes to fiscal policy will likely only offset retractions of monetary policy.

Just a thought.

In the meantime, here is what I am reading this weekend.

Trumponomics

- The Revolution That Failed by David Stockman via Daily Reckoning

- Sustaining The Trump Rally by Mohamed El-Erian via Project Syndicate

- Trumponomics Vs. Reality by Martin Feldstein via WSJ

- Can Trump Really Rebuild America by David Millward via The Telegraph

- Better Come To Terms With Growth Expectations by Eric Bush via GaveKal

- Trumpflation Is Coming! Really! by Kenneth Rapoza via Forbes

- Trumponics Gets Wall St Thumbs Up by Heather Long via CNN Money

- Lessons For Trump From JFK by Ray Keating via Real Clear Markets

- The Trouble With Trump’s Infrastructure Plan by Tyler Cowen via Bloomberg

- Trump May Have Trouble With Jobs Promise by Ana Swanson via WashPo

- Trump Can’t Fix The Economic Problem by Marc Levinson via Harvard Business Review

- Donald Trump & The New Economic Order by Michael Spence via Project Syndicate

- We’re All Populists Now by Dr. Ed Yardeni via Yardeni Research

- Q3 GDP Got Lots Of Temporary Help by Richard Moody via Regions

- The Big Infrastructure Myth by Marc Scribner via Foundation For Economic Freedom

Markets

- The “Ideal Buy High/Sell Low” Situation by Shawn Langlois via MarketWatch

- Market Could Soar 400-Points & Be A Bad Thing by Business Insider

- Buffett Indicator Says Stocks Overvalued by John Reese via CNBC

- Why The Bulls Will Stay In Charge by Howard Gold via MarketWatch

- Trump Will Benefit Almost All Stocks by Julie Verhage via Bloomberg

- Are The Markets All Wrong About Trump? by James Mackintosh via WSJ

- 3 Tailwinds To Buoy Global Stocks by Sid Verma & Blaise Robinson via Bloomberg

- Don’t Believe The Great Great Bond Fake-Out by Jeff Reeves via MarketWatch

- Global Bond Yields At A Glance by Peter Tchir via Forbes

- No Long-Term Issues For Bonds…YET by Michael Kahn via Barron’s

- Bond Market Trumpdado by Ivan Martchev via MarketWatch

- Inside Markets Love Affair With Trump by Charles Gasparino via New York Post

- 5% Yearly Returns Wishful Thinking by John Coumarianos via MarketWatch

- Just How Bullish IS The Market Right Now via Avi Gilburt via MarketWatch

- In Defense Of Fed’s Rate Hike Campaign by Edward Harrison via Credit Writedowns

Interesting Reads

- The Italian Connection by Danielle DiMartino-Booth via Money Strong

- 3-Signs Black Friday Was A Bust by Craig Wilson via Daily Reckoning

- The Best Credit Cards For 2016 by Brendan Harkness via Credit Card Insider

- Boomers & Gen-X’rs Are Worried by Rodney Brooks via WashPo

- Krugman On The Working Class by Tim Duy via Fed Watch

- Rates Will Remain Low by David Trainer via Forbes

- From Peak Oil To Peak Demand by Justin Fox via Bloomberg

- If You Build It (Infrastructure), They Won’t Come by Stephen Entin via IBD

- House Price Increases Less Than You Think by Keith Jurow via Advisor Perspectives

- Home Prices Reach New Highs, Houston Falls by Aaron Layman via AaronLayman.com

- Missing The Big Economic Picture by J Bradford Delong via Project Syndicate

- More Blowoff Than Breakout by John Hussman via Hussman Funds

- Are Industrial Metals Pointing To Economic Growth? by Dana Lyons via Tumblr

- Bonds Haven’t Priced In Trumpflation Yet by Jesse Felder via The Felder Report

“I am altering the deal. Pray I don’t alter it any further.” — Darth Vadar

*********

TLB recommends other pertinent articles at Real Investment Daily

*********

Find out about our great new TLB Project Membership package and benefits, add your voice and help us to change the world!

Find out about our great new TLB Project Membership package and benefits, add your voice and help us to change the world!

Leave a Reply