Governments Cannot Blame Inflation On Energy Anymore

By Daniel Lacalle

At the end of February 2023, the price of oil (WTI and Brent), Henry Hub and ICE natural gas, aluminum, copper, steel, corn, wheat, and the Baltic Dry Index are below the February 2022 levels.

The Supply Chain Index and the global supply-demand balance, published by Morgan Stanley, have declined to September 2022 levels. However, the latest inflation readings are hugely concerning.

Considering the previously mentioned prices of commodities and freight, if inflation were a “cost-push” phenomenon, it would have collapsed to 2% levels already. However, both headline and core inflation measures, from the Consumer Price Index (CPI) to Personal Consumer Expenditure Prices (PCE) show extremely elevated levels and rising core inflationary pressures.

We have mentioned numerous times that there is no such thing as “cost-push” inflation. It is only more units of currency going toward relatively scarce goods and services.

The monetary aspect of inflation has been proven on the way up and in the commodity correction. The Federal Reserve’s rate hikes have deflated the price of commodities despite rising geopolitical tensions, supply challenges, and robust demand growth. Rate hikes make it more expensive to store, take long positions, and finance margin calls. Powell offset the entire supply-demand tightness impact on prices.

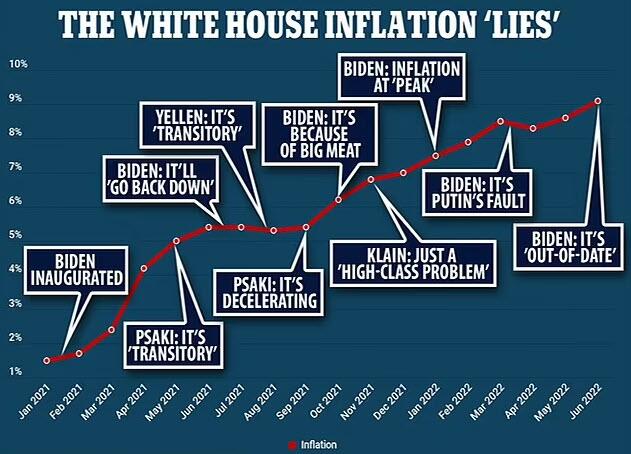

Governments cannot blame inflation on Putin’s war or the so-called “supply chain disruptions” anymore. Printing money above demand is the only thing that makes prices rise in unison. If a price rises due to an exogenous reason but the quantity of currency remains equal, all other prices do not rise. A PCE index of 4.5% in January 2023 with all the main commodities below the January 2022 level shows how high inflationary pressures are.

Inflation is accumulated, and the narrative is trying to convince us that bringing down inflation from 8% to 5% in 2024 will be a success. No. It will be a massive destruction of more than 20% of purchasing power of citizens from inflation in the period.

However, rate hikes are not enough. Broad-based money growth needs to come down rapidly. So far, in the United States, broad money growth is flat and has declined to more reasonable levels in December 2022. However, the latest ECB reading of broad money growth in the euro area points to a 4.1% increase, which is very high compared to modest gross domestic product (GDP) growth and certainly very high compared with the estimates for 2023.

Broad money growth was too aggressive in 2022 and it may take some time to ease the inflationary pressures to a level that does not make citizens even poorer.

Two recent papers published by the Bank of International Settlements remind us that money growth was the main culprit for the inflation surge. Borio, Hoffmann and Zakrajzek conclude that “a link can also be seen in the recent possible transition from a low- to a high-inflation regime. An upsurge in money growth preceded the inflation flare-up, and countries with stronger money growth saw markedly higher inflation. Looking at money growth would have helped to improve post-pandemic inflation forecasts, suggesting that its information value may have been neglected” (Does money growth help explain the recent inflation surge?). Reis explains that “Inflation rose because central banks allowed it to rise. Rather than highlighting isolated mistakes in judgment, this paper points instead to underlying forces that created a tolerance for inflation that persisted even after the deviation from target became large” (The burst of high inflation in 2021–22: how and why did we get here?)

The supply chain and Ukraine war excuse has vanished, but inflation remains too high. Many market participants want rate cuts and money supply growth to see higher markets, with multiple and valuation expansion. However, rate cuts are very unlikely in this scenario and central banks know they have caused a problem that will take more time than expected to correct.

Governments cannot expect inflation to correct when public spending is rising, which means higher consumption of new monetary units via deficit and debt.

Citizens are suffering these inflationary pressures via weakening real wage growth added to much higher cost of living as the prices of non-replaceable goods and services—education, healthcare, rents, and essential purchases—are rising much faster than the headline CPI suggests.

We are all poorer, and the headline is slightly lower. CPI does not mean lower prices, just a slower pace of destruction of the purchasing power of currencies.

Someone will invent another excuse to blame inflation on anything except the only thing that causes prices to rise at the same time: printing currency well above demand.

*********

(TLB) published this article by Daniel Lacalle as posted by Tyler Durden at ZeroHedge. Some emphasis and pictorial graphics were added by Tyler Durden

About Daniel Lacalle

Daniel Lacalle (Madrid, 1967). PhD Economist and Fund Manager. Author of bestsellers “Life In The Financial Markets” and “The Energy World Is Flat” as well as “Escape From the Central Bank Trap”. Daniel Lacalle (Madrid, 1967). PhD Economist and Fund Manager. Frequent collaborator with CNBC, Bloomberg, CNN, Hedgeye, Epoch Times, Mises Institute, BBN Times, Wall Street Journal, El Español, A3 Media and 13TV. Holds the CIIA (Certified International Investment Analyst) and masters in Economic Investigation and IESE. View all posts by Daniel Lacalle

Header featured image (edited) credit: Putin’s Price Hike/orginal ZH post

Some emphasis added by (TLB) editors

••••

••••

Stay tuned to …

••••

The Liberty Beacon Project is now expanding at a near exponential rate, and for this we are grateful and excited! But we must also be practical. For 7 years we have not asked for any donations, and have built this project with our own funds as we grew. We are now experiencing ever increasing growing pains due to the large number of websites and projects we represent. So we have just installed donation buttons on our websites and ask that you consider this when you visit them. Nothing is too small. We thank you for all your support and your considerations … (TLB)

••••

Comment Policy: As a privately owned web site, we reserve the right to remove comments that contain spam, advertising, vulgarity, threats of violence, racism, or personal/abusive attacks on other users. This also applies to trolling, the use of more than one alias, or just intentional mischief. Enforcement of this policy is at the discretion of this websites administrators. Repeat offenders may be blocked or permanently banned without prior warning.

••••

Disclaimer: TLB websites contain copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to our readers under the provisions of “fair use” in an effort to advance a better understanding of political, health, economic and social issues. The material on this site is distributed without profit to those who have expressed a prior interest in receiving it for research and educational purposes. If you wish to use copyrighted material for purposes other than “fair use” you must request permission from the copyright owner.

••••

Disclaimer: The information and opinions shared are for informational purposes only including, but not limited to, text, graphics, images and other material are not intended as medical advice or instruction. Nothing mentioned is intended to be a substitute for professional medical advice, diagnosis or treatment.

Leave a Reply