ER Editor: This is a rather long article by Sayer Ji on the privatized structural and funding network created around the possibility of a pandemic. But worth it. Everything ran through Epstein-as-intermediary.

🚨EPSTEIN FILES REVEAL POSSIBLE BILL GATES-EPSTEIN-JPMORGAN NETWORK FOR PANDEMIC/VACCINE PROFITEERING

2011: JPMorgan executives email Jeffrey Epstein asking for guidance on structuring a Bill Gates–linked donor-advised fund. In those emails, Epstein pushes language about… https://t.co/Wt5S0E0Jx1pic.twitter.com/JbkCKCA7vk

EPSTEIN FILES REVEAL POSSIBLE BILL GATES-EPSTEIN-JPMORGAN NETWORK FOR PANDEMIC/VACCINE PROFITEERING

2011: JPMorgan executives email Jeffrey Epstein asking for guidance on structuring a Bill Gates–linked donor-advised fund. In those emails, Epstein pushes language about “additional money for vaccines” and suggests creating an “offshore arm — especially for vaccines.”

2013: A Bill & Melinda Gates Foundation briefing describes the Global Health Investment Fund, targeting 5–7% financial returns on drug and vaccine development, backed by a 60% principal guarantee.

2015: The Gates Foundation corresponds with the International Peace Institute about pandemic preparedness discussions. IPI leadership had documented contact with Epstein.

January 2017: Text messages from Epstein’s phone describe “pandemic simulation” as a professional credential while discussing potential placements into Gates’ private office, pharmaceutical vaccine teams, and pandemic reinsurance roles.

March 2017: An internal planning document from Bill Gates’ private office (bgC3) lists “strain pandemic simulation” as a technical deliverable. The document was forwarded to Jeffrey Epstein.

May 2017: An email thread involving Epstein, Bill Gates, and Boris Nikolic references “pandemic” as a key long-term funding area.

October 2019: Event 201, co-hosted by the Gates Foundation, Johns Hopkins, and the World Economic Forum, simulates a novel coronavirus pandemic weeks before COVID-19 becomes public.

1/🚨 The DOJ just released thousands of pages of Epstein files.

And buried inside them may be one of the biggest bombshells no one is talking about:

The blueprint for a 20-year financial architecture designed to turn pandemics into a profit center.

BREAKING: The Epstein Files Illuminate a 20-Year Architecture Behind Pandemics as a Business Model—With Bill Gates at the Center of the Network

Inside the JPMorgan–Gates–Epstein Pipeline: Donor-Advised Funds, Vaccine Finance, and the Architecture of Pre-Positioned Profit

SAYER JI

Feb 02, 2026

The latest DOJ batch of Epstein files reveal that by the time the world encountered COVID-19, the financial, philanthropic, and institutional machinery to manage—and profit from—a pandemic was already firmly in place.

While the Epstein files have reignited scrutiny around specific relationships, their deeper significance lies in how they intersect with a much longer and largely unexamined timeline.

Public records, institutional initiatives, and financial instruments indicate that the conceptual foundations of pandemic preparedness as a managed financial and security category began to take shape in the late 1990s and early 2000s, as philanthropic capital, global health governance, and risk finance increasingly converged. Following the 2008 financial crisis, this framework rapidly accelerated—expanding through reinsurance markets, parametric triggers, donor-advised funding structures, and global simulations—years before COVID-19 made the architecture visible to the public.

What This Investigation Examines—and What It Does Not

This investigation is not concerned with the origins of COVID-19 itself. Rather, it examines what was already in place before it arrived. Drawing on internal emails, financial agreements, text messages, and planning documents—particularly from the 2011–2019 period, when many of these systems moved from conceptual to operational—the record shows that pandemics and vaccines were already being treated as standing financial and strategic categories. Investment vehicles, donor-advised fund structures, simulation programs, and reinsurance products were not improvised in response to crisis; they were refined and expanded within an architecture whose foundations predate the COVID-19 era by more than a decade.

Exercises such as Event 201 make clear that coronavirus pandemics were not hypothetical abstractions, but explicitly modeled scenarios—integrated into financial, philanthropic, and policy planning well before COVID-19 emerged.

Executive Summary

Vaccines as capital strategy: Internal JPMorgan emails from 2011 show Jeffrey Epstein advising the bank’s most senior executives on how to pitch a Gates-anchored donor-advised fund, insisting the presentation include the phrase “additional money for vaccines” and directing the creation of an “offshore arm — especially for vaccines.”

Pandemics as a funding vertical: A 2017 email thread between Epstein, Gates, and Boris Nikolic names “pandemic” as a “key area” for donor-advised fund structures—three years before COVID-19.

Pandemic simulation as career currency: A January 2017 iMessage thread from Epstein’s phone shows an associate listing “pandemics (just did pandemic simulation)” as a professional credential—while simultaneously discussing career placement into Gates’ private office, Boris Nikolic’s Biomatics Capital, Merck’s vaccine team, and Swiss Re’s pandemic reinsurance products.

Crisis as investable asset: A Gates Foundation briefing describes the Global Health Investment Fund as an “impact investment” vehicle targeting five-to-seven percent returns on drugs and vaccines, backed by a sixty percent principal guarantee.

Simulation as technical deliverable: A 2017 internal scope document from bgC3, Gates’ private office, lists “strain pandemic simulation” alongside neurotechnology and national defense applications.

The pandemic preparedness network: A 2015 Gates Foundation letter confirms pandemic preparedness coordination with the International Peace Institute—led by Terje Rød-Larsen, a documented Epstein dinner guest—while Epstein separately feeds Rød-Larsen Gates’s public pandemic messaging.

Prologue: The Architecture You Weren’t Meant to Notice

Nobody builds a fire station after the fire. That would be reactive. What the documents below reveal is something different—something closer to a fire stationbuilt beside a factory that stores accelerants, owned by the same people who wrote the building code.

The emails, agreements, text messages, investment briefings, and scope memos examined in this report do not prove that COVID-19 was manufactured or deliberately released. That is a separate evidentiary question. What they do show—in the participants’ own words—is that pandemics and vaccines were treated as standing financial and strategic categories years before any declared pandemic, complete with capital vehicles, legal frameworks, communications strategies, patent portfolios, simulation programs, reinsurance products, and rehearsal events.

The people building those structures were not public health officials reacting to emerging threats. They were financiers, private-office strategists, pharmaceutical executives, and convicted intermediaries working inside boardrooms at JPMorgan, drafting scope documents at Gates’ private office, coordinating across offshore jurisdictions, and brokering career placements into vaccine teams and pandemic reinsurance units.

That distinction matters. Preparedness is a public good. Pre-alignment of profit, power, and narrative control around a predicted crisis category is not—and the documents that follow show how easily such alignment drifts from public service into systemic exploitation.

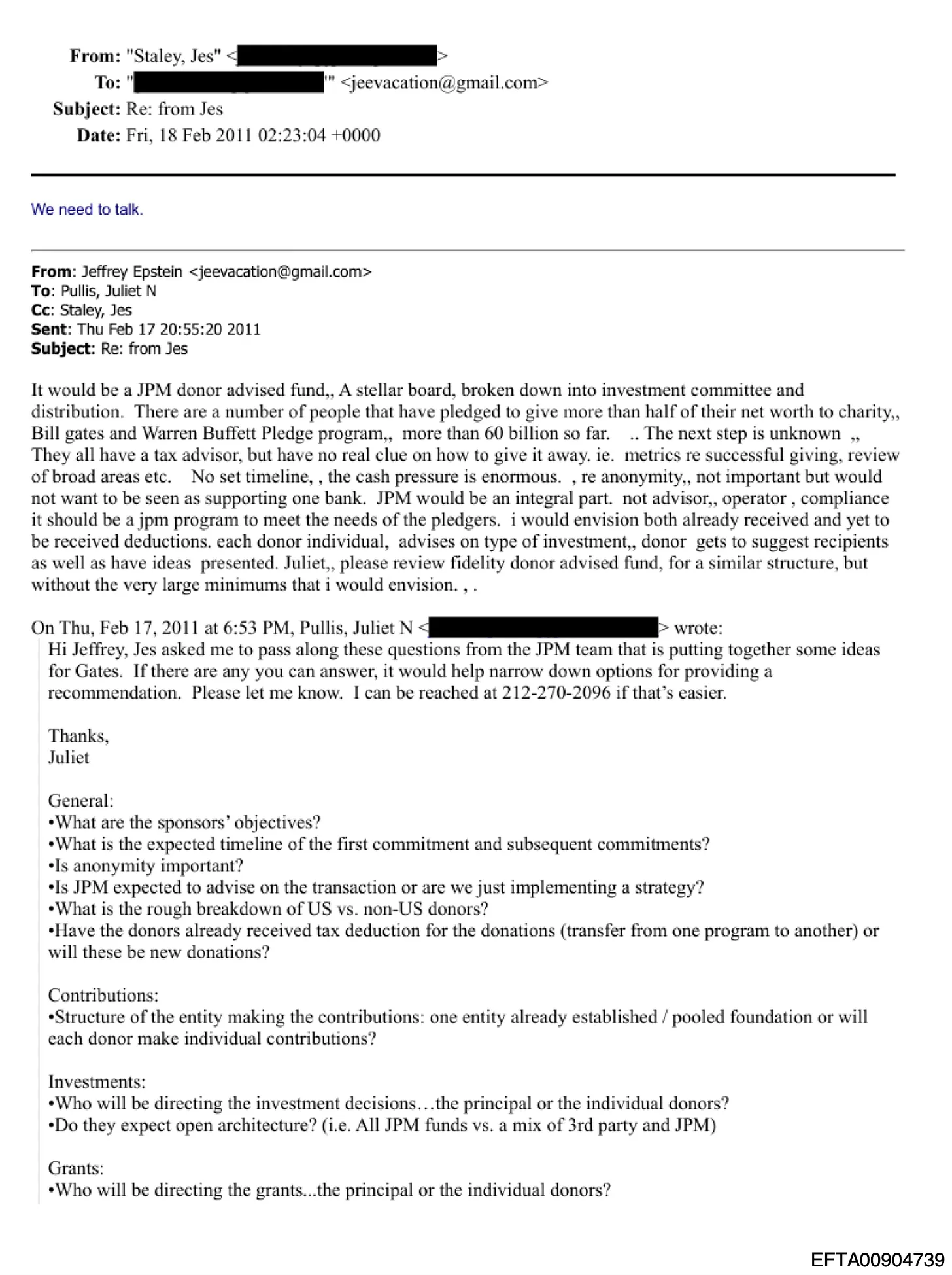

The Questionnaire: JPMorgan Comes to Epstein

Before the phrases that would later define this story—“money for vaccines,” “offshore arm,” “strain pandemic simulation”—there was a questionnaire. And the questionnaire tells you who was running things.

On February 17, 2011, Juliet Pullis, a JPMorgan executive working under Jes Staley, emailed Jeffrey Epstein with a structured list of questions. She explained that Staley had asked her to pass them along. The questions came from “the JPM team that is putting together some ideas for Gates.”

Source: Email thread titled “Re: from Jes” dated February 17–18, 2011. (EFTA00904739–40)

The questions were precise and operational: What are the sponsors’ objectives? Is anonymity important? Is JPMorgan expected to advise or implement? Who directs the investments—the principal or the individual donors? Who directs the grants? What technology platform is expected?

This is not a cold pitch. This is a major Wall Street bank asking a convicted sex offender to define the architecture of a Gates-linked charitable fund. JPMorgan wasn’t offering Epstein a seat at the table. They were asking him to design the table.

Epstein’s reply, sent the same evening, is remarkably fluent. He describes a JPMorgan donor-advised fund with a “stellar board, broken down into investment committee and distribution.” He references the Giving Pledge—the Gates-Buffett program in which billionaires commit to giving away more than half their net worth—and notes that more than sixty billion dollars had already been pledged. Then he identifies the opening:

“The next step is unknown. They all have a tax advisor, but have no real clue on how to give it away.”

He describes the fund’s relationship to the bank in language that goes well beyond advisory: “JPM would be an integral part. Not advisor… operator, compliance.” He envisions the bank not as a consultant recommending options, but as the operational backbone of the vehicle—handling compliance, administration, and investment execution.

Jes Staley’s response to all of this was two words: “We need to talk.”

The Sentence That Should Stop You Cold

Five months later—in July 2011—Epstein sent an internal email to Jes Staley, with Boris Nikolic, Bill Gates’ chief science and technology advisor, now copied. The email describes the proposed donor-advised fund in more developed terms. Buried in the operational language is a phrase worth reading twice:

“A silo based proposal that will get Bill more money for vaccines.”

Source: Email titled “GATES…” dated July 26, 2011 (EFTA01860211.pdf)

Not “more research.” Not “emergency capacity.” Not “public health resilience.” Money. For vaccines. That is the language of capital formation, not charity.

The CEO’s Questions, the Convict’s Answers

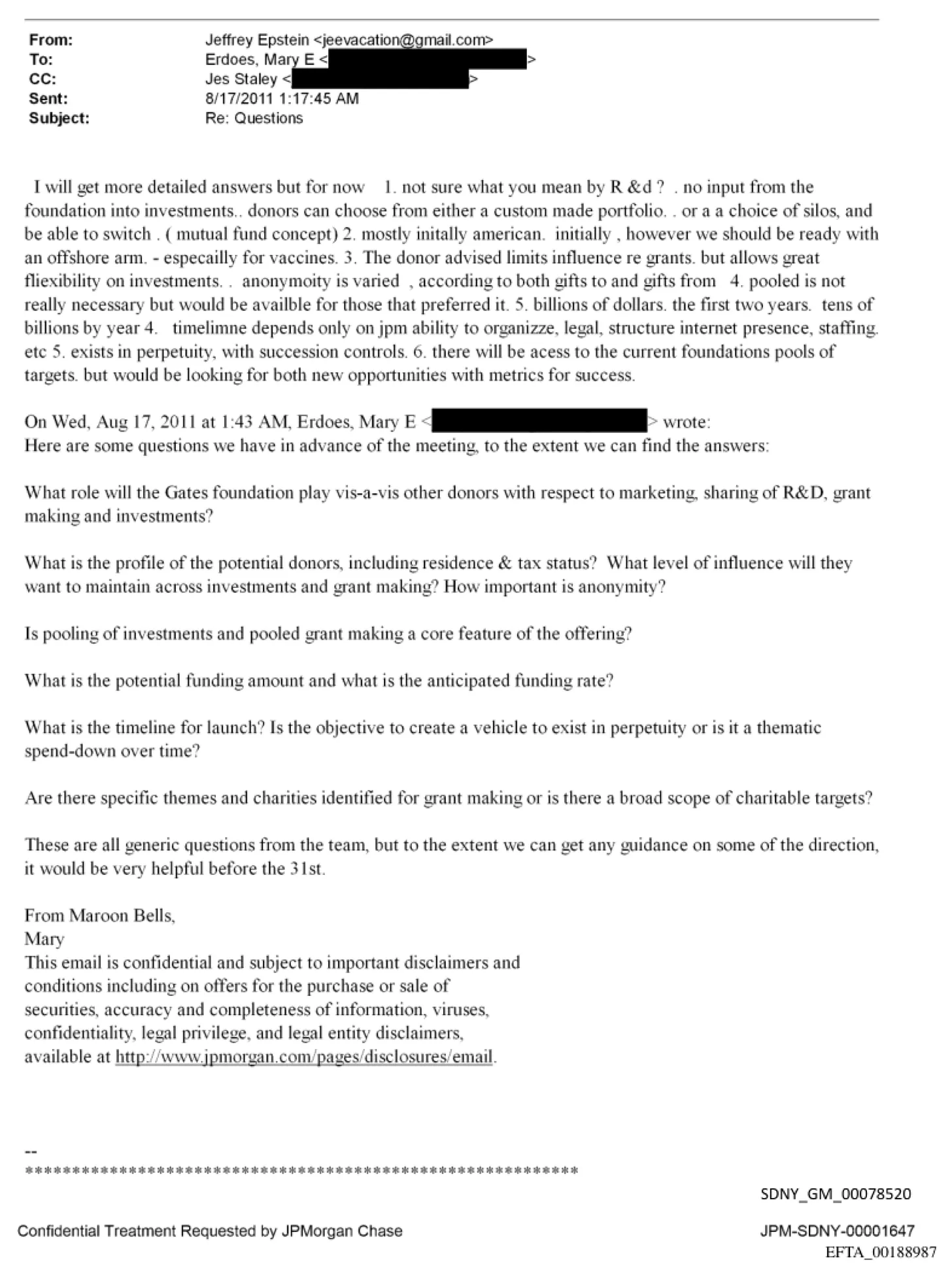

Three weeks later, on August 17, 2011, Mary Erdoes—CEO of JPMorgan Asset and Wealth Management—emailed Epstein directly with a second set of structured questions in advance of an upcoming meeting. She was writing from Maroon Bells, Colorado—on vacation—and cc’d Jes Staley.

Her questions were precise: What role will the Gates Foundation play vis-à-vis other donors? What is the profile of potential donors, including tax status? How important is anonymity? Is pooling of investments a core feature? What is the potential funding amount? What is the timeline for launch?

Source: Email titled “Re: Questions” dated August 17, 2011. (EFTA01256269)

Epstein’s reply, sent within minutes, is sweeping. No foundation input on investments. Donors choose from custom portfolios or predefined silos—a mutual fund concept. The fund would be “mostly initially American” but, he adds:

“However we should be ready with an offshore arm — especially for vaccines.”

He projects “billions of dollars” in the first two years and “tens of billions by year 4.” The timeline, he says, “depends only on JPM ability to organize, legal, structure, internet presence, staffing.” The bottleneck is not Gates. It is not the donors. It is the bank’s capacity to build what Epstein has already designed.

The fund wouldexist in perpetuity, with succession controls. Not a thematic spend-down. Not a time-limited initiative. A permanent vehicle—designed to outlive its creators.

And he adds that the fund would have “access to the current Foundation’s pools of targets” while also “looking for both new opportunities with metrics for success.” In a single email, Epstein has sketched a vehicle with global reach, offshore flexibility, perpetual duration, and direct access to the Gates Foundation’s pipeline.

The CEO of JPMorgan’s $2 trillion asset management division did not ask compliance to review this. She did not flag the source. She asked for answers before the 31st—and she got them the same night, from a man whose email signature read: “It is the property of Jeffrey Epstein.”

The Tension: Making Money from a Charitable Organization

Eleven days later, on August 28, 2011, Epstein sent a follow-up email to Staley and Erdoes outlining the donor-advised fund concept in even greater detail. The structure he describes is not a typical charitable vehicle. It is a financial platform:

The fund would be tied “initially just to the Gates program.” Minimum gift: one hundred million dollars. Projected scale: one hundred billion dollars within two years. The structure would include advisory boards, investment committees, grant committees, administration mirroring a mutual fund, valuation services for illiquid or “funky assets,” and investment management farmed out to Highbridge—a JPMorgan-affiliated hedge fund.

Then comes the line that acknowledges the contradiction at the center of the entire apparatus:

“The tension is making money from a Charitable Org. Therefore the money making parts need to be arms length.”

The architect of this structure—a man convicted of sex crimes against minors—is explicitly acknowledging that the vehicle is designed to generate profit under the legal cover of charity. His proposed solution is not to eliminate the profit motive but to obscure it through “arm’s length” separation.

“Bill Is Terribly Frustrated”

The same August 2011 email chain contains another revealing passage. Epstein, writing to Erdoes, describes Gates’ emotional state regarding the pace of the project:

“Bill is terribly frustrated. He would like to boost some of the things that are working without taking away from those that are not… therefore, explaining that this would allow ‘additional money for vaccines’ must be included in the presentation.”

Source: Email titled “Re: Questions” dated August 17, 2011. (EFTA01301108)

This sentence tells us four things at once. First, Epstein is speaking with direct knowledge of Gates’ internal emotional state. Second, he is shaping JPMorgan’s presentation strategy. Third, vaccine funding is the hook—the narrative justification for the financial structure. And fourth, Epstein is the one dictating what “must be included” to close the deal.

In the same correspondence, Epstein describes the Gates Foundation as “a very very sensitive bunch that has spent billions… there is little that can be held up as a great success and even polio is not yet finished.” This is not philanthropy analysis. It is client management. Epstein is coaching a Wall Street executive on how to handle a billionaire’s insecurities.

Why Donor-Advised Funds Matter

A brief clarification for readers unfamiliar with the financial architecture at the center of this story.

Donor-advised funds are not illegal or inherently abusive. They are widely used charitable vehicles that allow donors to receive an immediate tax deduction while retaining advisory influence over how their contribution is invested and eventually distributed as grants. Fidelity, Schwab, and Vanguard all operate DAFs. They are mainstream.

What makes them relevant here is scale, opacity, and timing. When DAFs are designed for perpetual duration, offshore flexibility, hundred-million-dollar minimums, and investment-first logic—when their stated purpose is not merely charitable giving but the generation of returns through vehicles like hedge funds and structured products—they blur the line between philanthropy and financial engineering in ways public oversight rarely penetrates.

The tax benefit is immediate. The charitable distribution can be deferred indefinitely. And the investment returns generated in the interim accrue inside a tax-exempt structure. When Epstein writes that “the tension is making money from a charitable org” and proposes “arm’s length” separation as the solution, he is describing not an abuse of the system but the system working exactly as designed—at a scale most regulators never anticipated.

Impact Investing: When Crisis Becomes an Asset Class

If the 2011 emails show the pitch, a separate Gates Foundation briefing document reveals the philosophy in its mature form.

A confidential 15-page briefing prepared for a JPMorgan-hosted panel on September 23, 2013, describes the Global Health Investment Fund as “the first investment fund focused on global health drug and vaccine development.” The fund explicitly targets financial returns in the range of five to seven percent, while returning all investor capital.

Source: Briefing titled “JPM Panel – Launch of the Global Health Investment Fund.” (0EFTA01103797)

The mechanism for de-risking private investment is critical: the Gates Foundation and other partners provide a sixty percent guarantee of principal, meaning investors could participate in vaccine and drug development with the majority of their downside absorbed by philanthropic and sovereign capital.

This is the structural logic of pandemic finance laid bare: public risk, philanthropic backstop, private upside. Vaccines and global health tools are reframed not as public goods to be funded and forgotten, but as investable assets whose risk profiles are deliberately engineered for capital participation.

The Pandemic Preparedness Network: Gates, Epstein, and the International Peace Institute

The article’s previous sections follow the money. This one follows the meeting invitations—and they lead to the same places.

On March 9, 2015, Amy K. Carter, Deputy Director of Family Interest Grants at the Bill & Melinda Gates Foundation, wrote to Dr. Terje Rød-Larsen, President of the International Peace Institute, regarding IPI’s proposal for “a convening of experts to discuss how we can most effectively address and prevent pandemics.”

Source: Gates Foundation letter to IPI. March 9, 2015. (EFTA02713880 / EFTA_R1_02137620)

The Foundation declined to fund the convening but confirmed that many of the groups in IPI’s proposal were “already in discussions with Gates Foundation staff about pandemic preparedness and response” in the lead-up to the World Health Assembly and G7. The letter noted these would be “key topics” at both forums.

Now recall: Rød-Larsen is the same man who attended the September 2013 dinner at Epstein’s residence alongside both Bill and Melinda Gates and Thorbjørn Jagland, then Secretary-General of the Council of Europe. This is not a tangential connection. Rød-Larsen’s institution is proposing pandemic convenings to Gates—and his private social life runs through Epstein’s dining room.

Three months later, on June 2, 2015, Epstein forwarded Rød-Larsen a Vox article about Bill Gates and flu pandemic preparedness—without comment, just the link. The URL: vox.com/2015/5/27/8660249/gates-flu-pandemic.

Source: Email from Jeffrey Epstein to Terje Rød-Larsen. June 2, 2015. (EFTA02499005)

The pattern is precise: Gates’s Foundation declines to fund Rød-Larsen’s pandemic convening in March. Epstein sends Rød-Larsen Gates’s public pandemic messaging in June. The institutional channel says no. The Epstein channel keeps the line open.This is the function of an intermediary: maintaining relationships that formal institutions cannot—or will not—maintain themselves.

From Proposal to Power: The May 2015 Geneva Pandemic Preparedness Convening

The proposal did not remain theoretical. In May 2015, the International Peace Institute convened a closed-door, high-level meeting in Geneva titled “Preparing for Pandemics: Lessons Learned for More Effective Responses.”The agenda reveals a convergence of institutional power rarely assembled outside moments of declared crisis: the Director-General of the World Health Organization, the President of the World Bank, the President of the International Committee of the Red Cross, the International President of Médecins Sans Frontières, and senior UN and global health officials.

Notably, the agenda for this Geneva convening circulated privately in advance, referenced explicitly in a March, 20th 2015 Epstein email from International Peace Institute leadership and forwarded through diplomatic channels weeks before the meeting convened—underscoring that this convergence was planned, coordinated, and deliberate rather than emergent.

The framing of the meeting is itself revealing. Rather than focusing narrowly on epidemiology or retrospective analysis, the agenda is structured around forward-looking governance questions: how pandemics should be anticipated, how authority should be exercised, how multiple stakeholders should be coordinated, and—critically—what legal, institutional, and financial mechanisms must be put in place in advance to enable rapid, centralized response. One full session is dedicated to identifying legal and managerial gaps, institutional bottlenecks, and pressure points that had constrained prior responses, followed by another focused explicitly on implementation: who should be responsible, how policies should be operationalized, and how international follow-through should occur.

In this context, pandemic preparedness is not treated as contingency planning for rare events, but as a standing domain of global governance—one requiring pre-aligned authority, pre-established chains of responsibility, and ready financial instruments. The presence of the World Bank alongside humanitarian and health institutions underscores that pandemics were already being conceptualized not only as public health crises, but as systemic shocks demanding coordinated financial and policy response.This architecture was being assembled years before COVID-19, and long before the public would be invited into any meaningful debate about its scope, legitimacy, or consequences.

Source: International Peace Institute. “Preparing for Pandemics: Lessons Learned for More Effective Responses” (Agenda). Geneva, May 2015. (EFTA_R1_01347204)

Pandemic as a Category—Not an Event

In May 2017, an email thread involving Epstein, Gates, and Boris Nikolic returns to the donor-advised fund concept. Epstein frames DAFs as a “counter balance” to anticipated cuts in public science funding. Nikolic responds with a line that deserves to be read slowly:

“It might be a great path forward for some key areas such as Energy, pandemic etc.”

Source: Email thread dated May 24, 2017. (EFTA00697005)

Pandemic is listed as a standing category—equivalent to energy—suitable for long-term private capital mobilization. This is not the language of emergency response. It is the language of portfolio strategy.

By 2017, three years before COVID-19, the people closest to Gates were already treating pandemics as a durable funding vertical—a domain that would persist regardless of whether a specific outbreak materialized.

The Rolodex: Pandemic Simulation as Career Currency

The most startling document in this batch is not an email to a bank executive or a foundation letter. It is a text message thread—an iMessage conversation from Epstein’s phone, dated January 20–23, 2017—between Epstein (using the handle [email protected]) and an unidentified associate.

Source: iMessage thread, January 20–23, 2017. (EFTA01617419–27)

The conversation begins with a birthday greeting. The associate is flying in from Zurich. They arrange a brief meeting. Then the conversation shifts into something extraordinary: a career-planning session in which the associate maps out their professional options—and nearly every path runs through Epstein’s network.

The associate’s self-description is remarkable in its specificity. They describe themselves as a physician with experience at the UN, WHO, Gates Foundation, and World Bank. And then:

“Also my expertise is public health security. Pandemics (just did pandemic simulation) and threats to US health. That could be big platform.”

Pandemic simulation is being treated as a career credential—a professional asset to be leveraged for placement. Not a public safety exercise. Not an academic undertaking. A “platform” for career advancement, mentioned in the same breath as political access and institutional power.

The career options the associate then lists read like a map of the pandemic-preparedness industrial complex:

“Board partner at Biomatics Capital (Boris) but would mean I have to help him raise funds from BG.”

Biomatics Capital is Boris Nikolic’s venture fund. Nikolic—Gates’ chief science advisor, the same man cc’d on the 2011 vaccine emails, the same man who would later list “pandemic” as a DAF category—is here receiving personnel brokered through Epstein.

“BG office (for 6 months max) working on a series of messy agendas but as his senior science advisor.”

Gates’ private office—bgC3, the same entity that produced the “strain pandemic simulation” deliverable—is listed as a landing spot. Epstein’s role as gatekeeper is explicit. He later instructs: “Put together your resume… for my submission.”

“Join Merck team for 6–12 months in their vaccine team (big push for gardasil vaccine/HPV) would have to base in Rwanda.”

Merck’s vaccine team. Gardasil. A direct pipeline from Epstein’s phone to pharmaceutical vaccine operations.

“Join Swiss Re (reinsurance) team developing health products. Did one for pandemics, helped develop parametric trigger.”

This is perhaps the most structurally significant entry on the list. Swiss Re is one of the world’s largest reinsurance companies. A “parametric trigger” is an automated financial mechanism that pays out when a predefined threshold is crossed—in this case, a pandemic declaration. The associate is describing having helped develop a financial product thatautomatically generates payouts when a pandemic is declared. And Epstein’s network is the career placement vehicle.

The associate also mentions:

“Join the World Economic Forum as chief science advisor to Klaus Schwab.”

And:

“Join Martin Sorrell team and help develop media tech to understand and counteract international Gov’t fragility.”

The full list spans Gates’ office, Nikolic’s fund, Merck’s vaccine team, Swiss Re’s pandemic products, the World Economic Forum, the Rockefeller Foundation, the World Bank, Goldman Sachs, Alibaba, MasterCard, and TPG Capital. Every major node in the pandemic-preparedness-to-profit pipeline appears on a single career menu—brokered through Jeffrey Epstein’s text messages.

And then the associate reveals how Gates himself fits into the calculus:

“BG… He hates mental health but he’s crazy about vaccines and autism stuff. That could be start to a more broad conversation.”

Gates’s interest in vaccines is described not as a philanthropic commitment but as apsychological lever for access. The associate frames vaccines and autism as the entry point—the hook—that will open the door to “a more broad conversation.” This is the same strategic logic Epstein used in 2011 when he insisted “additional money for vaccines must be included” in the JPMorgan presentation. Vaccines are not the mission. They are the key.

Epstein’s response to this sprawling career inventory? “BG.” Then: “No too broad.” Then: “Bg.” He steers his associate toward Gates. The associate acquiesces. Epstein instructs: “Put together your resume… for my submission.”

One further line from this thread demands attention. The day before, Epstein had texted: “Feel free to ask Bill if he would like a private meeting with Bannon, Thiel, or Barrack.” This was January 21, 2017—the day after Donald Trump’s inauguration. Epstein is offering to broker private meetings between Bill Gates and the incoming administration’s power center. The man who designed the donor-advised fund, who directed JPMorgan’s presentation strategy, who placed personnel into Gates’ office and Nikolic’s fund, is now offering to connect Gates to the White House.

Strain Pandemic Simulation: A Technical Deliverable

Two months later—March 2017—a separate email titled “bgc3 Deliverables and Scope” outlines proposed work for bgC3, Bill Gates’ private strategic office. The document lists deliverables across several domains: domestic health, personal health data infrastructure, neurotechnology, brain science, and—listed without any special emphasis—

“Follow-up recommendations and/or technical specifications for strain pandemic simulation.”

Grouped alongside this are neurotechnologies as weapons in national intelligence and defense.

This is not a public tabletop exercise or a policy white paper. It is an internal scope document treating pandemic simulation as a technical discipline—one that sits within the same planning universe as health surveillance, data systems, and defense applications.

The email was forwarded to Jeffrey Epstein. Whatever his specific role, his continued visibility into Gates’ strategic planning as late as 2017 is documented—not inferred.

Combined with the January 2017 iMessage thread—in which an Epstein associate casually references having “just did pandemic simulation”—the picture becomes clear: pandemic simulation was not an occasional exercise. It was a standing capability, a career credential, and a technical deliverable within the Gates-Epstein orbit, all in the same quarter of the same year.

Between the March 2017 scope document and the October 2019 simulation, the architecture did not pause. It accelerated—through public channels now visible to anyone willing to look.

In January 2017—the same month as the iMessage career-planning thread and the same quarter as the bgC3 scope document—the Coalition for Epidemic Preparedness Innovations was formally launched at the World Economic Forum in Davos with $460 million in initial funding from the Gates Foundation, the Wellcome Trust, and the governments of Norway, Japan, and Germany. CEPI’s explicit mission: to reduce vaccine development timelines from ten years to under twelve months, with initial targets including MERS coronavirus. Gates described the initiative at Davos as building vaccine infrastructure “in peace time” so it would be ready when a pandemic arrived.

Six months later, in June 2017, the World Bank issued the first-ever pandemic catastrophe bonds—$320 million in securities sold to private investors through its Pandemic Emergency Financing Facility. The bonds were structured by Swiss Re and Munich Re, with parametric triggers that would automatically release capital when predetermined pandemic thresholds were crossed. Coronavirus was explicitly listed as a covered peril. Investors received coupon rates above eleven percent on the higher-risk tranche—returns that would continue as long as no qualifying pandemic occurred. When COVID-19 eventually triggered the bonds in April 2020, investors lost their principal and $195.84 million was disbursed. But for the preceding three years, the product had functioned exactly as the iMessage associate described: a pandemic reinsurance instrument with a parametric trigger, generating returns until the declared event arrived.

Meanwhile, in December 2019—weeks before the WHO was notified of the Wuhan pneumonia cluster—NIAID and Moderna executed a material transfer agreement sending mRNA coronavirus vaccine candidates to Ralph Baric’s laboratory at UNC Chapel Hill.

By the time Event 201 convened, the architecture documented in the preceding sections was no longer conceptual. It had been funded, structured, bonded, insured, staffed, and legally papered. What remained was the rehearsal.

Event 201: The Dress Rehearsal

On October 18, 2019—six weeks before the first publicly acknowledged cases of COVID-19—the Johns Hopkins Center for Health Security, the World Economic Forum, and the Bill & Melinda Gates Foundation co-hosted Event 201, a high-level pandemic simulation exercise featuring a novel coronavirus.

The exercise focused on government coordination, pharmaceutical supply chains, media management, social media censorship strategies, public compliance, and international governance alignment. Participants included representatives from global financial institutions, pharmaceutical companies, intelligence agencies, and media organizations.

Event 201 did not cause COVID-19. That is not the claim.

The claim is this: when a coronavirus pandemic is simulated weeks before a real coronavirus pandemic emerges, and when that simulation aligns with years of prior financial structuring, patent development, internal simulation work, reinsurance product development, personnel placement into vaccine teams, and capital vehicles already designed around pandemic-category returns—coincidence alone is an insufficient explanation for the convergence.

It does not prove conspiracy. It proves that the institutional infrastructure to capitalize on exactly this kind of crisis was already built, tested, staffed, and insured.

The Patent Foresight Problem

A note on evidentiary scope: the preceding sections of this investigation draw exclusively on internal emails, financial agreements, text messages, and planning documents from the Epstein files—primary source evidence in the participants’ own words. The patent record that follows is drawn from a different evidentiary category: publicly available filings with the United States Patent and Trademark Office and peer-reviewed scientific literature. No direct documentary link between the patent holders below and the Epstein-Gates-JPMorgan correspondence has been established in the released files. What the patent record does establish is the broader industrial context in which the financial architecture documented above was built—and the timeline that made rapid monetization structurally possible.

Long before COVID-19 was named, coronavirus-related technologies were being patented. The specifics are a matter of public record.

Moderna’s foundational mRNA patents claim priority to applications filed between 2010 and 2016. In 2015, NIAID and Moderna entered a cooperative research and development agreement focused on mRNA vaccine development. By December 12, 2019—weeks before the WHO was notified of a pneumonia cluster in Wuhan—a material transfer agreement between NIAID, Moderna, and Ralph Baric’s laboratory at the University of North Carolina at Chapel Hill transferred “mRNA coronavirus vaccine candidates developed and jointly owned by NIAID and Moderna” for animal testing. That agreement was specific to MERS-CoV, not SARS-CoV-2, and was amended in February 2020 after the new virus was sequenced. But the platform was already built.

The patent trail at UNC is older still. Ralph Baric filed his first patent on methods for producing recombinant coronavirus in April 2002 (US Patent No. 7,279,327). In March 2015, Baric and colleagues filed an international patent application for chimeric coronavirus spike proteins (PCT/US2015/021773), granted as US Patent No. 9,884,895 in February 2018—funded under NIH Grant No. U54AI057157. Baric’s decades of NIH-funded coronavirus research, including gain-of-function work on spike protein constructs, produced capabilities that were extensively documented in peer-reviewed literature and patent filings years before 2020.

These patents do not prove intent to release a pathogen. That is not the claim. They prove anticipation of utility—and they enabled rapid monetization when the anticipated conditions materialized, a dynamic recognized in intellectual property law as patent foresight. (See The Patent Foresight Problem: https://www.lexology.com/library/detail.aspx?g=1a4573cc-01b7-4da3-b5e9-739c60d0c9ee)

The structural point is this: the financial architecture documented in the preceding sections—the DAFs, the impact investment vehicles, the reinsurance triggers, the simulation programs—was not built in a vacuum. It was built alongside, and in some cases directly adjacent to, a patent and technology development pipeline that ensured whoever controlled the platform would be positioned to move first when a coronavirus pandemic materialized. The documents examined in this investigation do not prove that these two tracks were coordinated. They prove that they were concurrent, that they involved overlapping institutions, and that both were fully operational before COVID-19 arrived.

When patents, simulations, capital vehicles, rehearsal events, reinsurance triggers, and internal scope documents all exist before a crisis, what you are looking at is not a conspiracy theory. It is structural readiness for profit—the kind of readiness that rewards speed, centralizes control, and marginalizes alternative approaches.

Patents associated with Moderna for coronavirus vaccine platforms existed years before the pandemic. Research conducted by Ralph Baric and colleagues at the University of North Carolina, in collaboration with NIH-funded laboratories, produced coronavirus spike protein research and gain-of-function capabilities that were documented in peer-reviewed literature and patent filings well before 2020.

Patents do not prove intent to release a pathogen. They prove anticipation of utility—and they enable rapid monetization when the anticipated conditions materialize, a dynamic recognized in intellectual property law as patent foresight.

(See The Patent Foresight Problem: https://www.lexology.com/library/detail.aspx?g=1a4573cc-01b7-4da3-b5e9-739c60d0c9ee)

Epstein as Intermediary: Governance Risk, Not Gossip

Among the most consequential documents in this archive is an agreement letter dated August 8, 2013, addressed to William H. Gates.

The letter states that Gates “specifically requested” that Jeffrey Epstein “personally serve as the representative” of Boris Nikolic in certain financial and logistical negotiations. It acknowledges that Epstein had an “existing collegial relationship” with Gates, in which Epstein had already received “confidential and/or proprietary information.” Gates waives conflicts of interest and provides broad indemnification.

Source: Agreement letter dated August 8, 2013. (EFTA02685163)

This agreement was executed five years after Epstein’s conviction for soliciting a minor for prostitution. Gates had the resources to work with anyone on earth. He chose a registered sex offender—and put it in writing.

Additional scheduling records from 2010 through 2014 document repeated private meetings, dinners, private jet travel, late-night appointments, and a September 2013 dinner at Epstein’s residence attended by both Bill and Melinda Gates, alongside Terje Rød-Larsen and Thorbjørn Jagland—the same Rød-Larsen whose International Peace Institute was coordinating pandemic convenings with the Gates Foundation, and who received Epstein’s pandemic-related media forwards.

And as the January 2017 iMessage thread demonstrates, Epstein’s intermediary function extended well beyond Gates personally. He was placing personnel into Gates’ private office, Nikolic’s Biomatics Capital, Merck’s vaccine team, Swiss Re’s pandemic reinsurance unit, and the World Economic Forum. He was brokering meetings with the incoming Trump administration. He was directing presentation strategy at JPMorgan. He was, in short, the human router through which pandemic-adjacent finance, science, policy, and political access all flowed.

Intermediaries matter because they shape outcomes without accountability. When a figure with Epstein’s record sits at the center of this web, public trust is not an externality—it is a casualty.

The issue is not merely that Epstein was involved, but that institutions with unlimited resources repeatedly chose him as an intermediary—despite his conviction—when other options were abundant. JPMorgan had thousands of wealth advisors. The Gates Foundation had a staff of over 1,500. Boris Nikolic could have retained any law firm in the country. They chose Epstein—and they kept choosing him, year after year, from 2011 through at least 2017. That pattern reflects a governance failure, not a coincidence.

Reading Between the Lines

Here is what these documents, taken together, reveal—not as accusation, but as pattern:

JPMorgan treated a convicted sex offender as the operational architect of a Gates-linked charitable fund—soliciting his input on structure, compliance, and strategy as early as February 2011.

Vaccines were positioned as a capital-raising narrative inside financial structures designed for scale, offshore flexibility, and arm’s-length profit generation—years before any pandemic.

Pandemic was treated as a standing strategic category—not a hypothetical emergency—by the people designing donor-advised funds and impact-investment vehicles.

Pandemic simulation was simultaneously a technical deliverable, a career credential, and a career-placement pathway—all within the Gates-Epstein orbit, all documented in early 2017.

Pandemic reinsurance products with parametric triggers—financial instruments that automatically pay out upon a pandemic declaration—were being developed by professionals in Epstein’s career-placement network.

The pandemic preparedness network ran through Epstein: from the Gates Foundation’s institutional correspondence with the International Peace Institute to Epstein’s private channel to its president.

Rehearsal events modeled not merely disease spread, but narrative control, government coordination, and public compliance—weeks before the real thing.

Financial structures guaranteed that private investors bore minimal risk while retaining upside—a design that creates systemic incentives to identify, maintain, and even prefer the conditions under which those investments pay off.

None of this requires criminal intent to be dangerous. The structural incentive alone—where preparedness, capital, power, and narrative converge before a crisis—creates a gravitational pull toward outcomes that serve the prepared.

The Innocent Explanation—and Its Limits

Defenders of these arrangements will argue that pandemic preparedness, simulation exercises, vaccine investment, and reinsurance products are simply prudent responses to known global risks. Pandemics have always been a matter of when, not if. Responsible institutions plan for them.

That argument deserves to be taken seriously—and at its strongest, not its weakest.

Donor-advised funds are not exotic. Fidelity Charitable is the largest grantmaker in the United States. DAF structures at the hundred-million-dollar scale are standard instruments for ultra-high-net-worth philanthropists, and the Gates Foundation is hardly the only organization to use them. The existence of a DAF, even a large and complex one, does not by itself indicate anything improper.

Nor was pandemic preparedness a fringe concern. Between 2000 and 2019, governments, multilateral institutions, academic centers, and private foundations across the world invested heavily in pandemic readiness. The WHO, the CDC, BARDA, the Wellcome Trust, the Coalition for Epidemic Preparedness Innovations, and dozens of universities ran simulations, funded vaccine platforms, and developed financing mechanisms—most with no connection to Jeffrey Epstein whatsoever. Pandemic preparedness was mainstream institutional activity, and many of the people engaged in it were acting in straightforward good faith.

All of this is true. And none of it answers the questions these documents raise.

The question is not whether DAFs exist or whether pandemic preparedness is legitimate. The question is why the specific architecture documented here—offshore arms earmarked for vaccines, perpetual-duration vehicles with arm’s-length profit separation, parametric triggers that automate payouts on pandemic declarations—was designed, refined, and operationalized through a channel that ran repeatedly through a convicted sex offender. The mainstream existence of these tools makes the routing more puzzling, not less. Gates had access to every law firm, every bank, every advisory structure on earth. JPMorgan had thousands of wealth advisors. Boris Nikolic could have retained any consultancy in the country. The abundance of legitimate alternatives is precisely what makes the exposed channel so difficult to explain away.

Nor does the breadth of legitimate pandemic preparedness explain the concentration documented here. Hundreds of institutions worked on preparedness. But the documents in this report do not describe hundreds of institutions. They describe a single network in which the same small group of individuals simultaneously designed the financial vehicles, directed the presentation strategy, placed personnel into vaccine teams and reinsurance units, funded the simulations, held the patents, and brokered political access—with one man serving as the connective tissue across all of these functions. The issue is not that preparedness happened. It is that so many of its financial, strategic, and personnel dimensions converged through a single, compromised intermediary.

Preparedness can be public. It can be transparent. It can be subject to democratic oversight. What these douments show is preparedness that was privatized, financialized, and insulated from accountability. The distinction between public-interest planning and private-interest pre-positioning is not semantic. It is the difference between a fire department and an arson investigator who also sells fire insurance.

The benign reading requires you to believe that every structural feature of this system—the offshore arms, the perpetual duration, the parametric triggers, the arm’s-length separation, the convicted intermediary—was simply good planning. The documents invite a different question: good planning for whom?

The Question No One Is Supposed to Ask

If systems are built to profit from crisis—if the same people who design the financial vehicles also fund the simulations, hold the patents, develop the reinsurance triggers, place the personnel, shape the policy, and manage the narrative—then the question is not whether they would act in their own interest.

The question is: what structural safeguard exists to ensure they don’t?

And if the answer is “trust”—trust in the same institutions that platformed a convicted sex offender as a financial intermediary, that structured charitable vehicles with acknowledged “tension” around profit, that simulated a coronavirus pandemic weeks before one arrived, that built reinsurance triggers designed to pay out on pandemic declarations—then trust alone is not enough.

Transparency is not cynicism. Accountability is not conspiracy theory. And asking who profits from catastrophe is the oldest and most necessary question in public life.

Sunlight remains the most effective public health intervention ever devised. It costs nothing. It requires no patent. And it has no side effects—except for those who prefer to operate in the dark.

1/🚨 The DOJ just released thousands of pages of Epstein files. And buried inside them may be one of the biggest bombshells no one is talking about: The blueprint for a 20-year financial architecture designed to turn pandemics into a profit center. Offshore vaccine funds.

8. Bill & Melinda Gates Foundation (Amy K. Carter) to Dr. Terje Rød-Larsen, International Peace Institute. Letter re: pandemic preparedness convening. March 9, 2015. (EFTA02713880 / EFTA_R1_02137620)

9. Jeffrey Epstein to Terje Rød-Larsen. Forwarded Vox article on Gates and flu pandemic preparedness. June 2, 2015. (EFTA02499005 / EFTA_R1_01624983)

10. iMessage thread from Epstein’s phone ([email protected]). Career planning, pandemic simulation, Gates access, vaccine/pharma placement. January 20–23, 2017. (EFTA01617419–27)

11. Email titled “bgc3 Deliverables and Scope.” March 3, 2017. Forwarded to Jeffrey Epstein.

12. Jeffrey Epstein, Bill Gates, and Boris Nikolic. Email thread re: DAF as counter-balance. May 24, 2017. (EFTA00697005)

13. Bill Gates to Jeffrey Epstein. Forwarded calendar invitation. “Billg Meeting w/Jeffrey Epstein (Boris)” at BMGF campus. July 2011.

14. Boris Nikolic to Jeffrey Epstein. “FW: Bio.” February 5, 2014.

15. Johns Hopkins Center for Health Security, World Economic Forum, and Bill & Melinda Gates Foundation. “Event 201 Pandemic Exercise.” October 18, 2019.

16. Moderna, Inc. Coronavirus vaccine platform patent filings prior to 2020. United States Patent and Trademark Office.

The Liberty Beacon Project is now expanding at a near exponential rate, and for this we are grateful and excited! But we must also be practical. For 7 years we have not asked for any donations, and have built this project with our own funds as we grew. We are now experiencing ever increasing growing pains due to the large number of websites and projects we represent. So we have just installed donation buttons on our websites and ask that you consider this when you visit them. Nothing is too small. We thank you for all your support and your considerations … (TLB)

••••

Comment Policy: As a privately owned web site, we reserve the right to remove comments that contain spam, advertising, vulgarity, threats of violence, racism, or personal/abusive attacks on other users. This also applies to trolling, the use of more than one alias, or just intentional mischief. Enforcement of this policy is at the discretion of this websites administrators. Repeat offenders may be blocked or permanently banned without prior warning.

••••

Disclaimer: TLB websites contain copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to our readers under the provisions of “fair use” in an effort to advance a better understanding of political, health, economic and social issues. The material on this site is distributed without profit to those who have expressed a prior interest in receiving it for research and educational purposes. If you wish to use copyrighted material for purposes other than “fair use” you must request permission from the copyright owner.

••••

Disclaimer: The information and opinions shared are for informational purposes only including, but not limited to, text, graphics, images and other material are not intended as medical advice or instruction. Nothing mentioned is intended to be a substitute for professional medical advice, diagnosis or treatment.

")

Leave a Reply