Biden’s Federal Land Lease Ban To Send Oil Prices Higher: Goldman

BY TYLER DURDEN

Oil stocks tumbled following [Thursday’s] one-two punch of Biden energy news, when first we learned that the Interior Department enacted a 60-day moratorium on issuing oil and gas leases that affects all federal lands, minerals, and waters, which was followed by news that Biden was set to fully suspend the sale of oil and gas leases on federal land, which accounts for about a tenth of U.S. supplies.

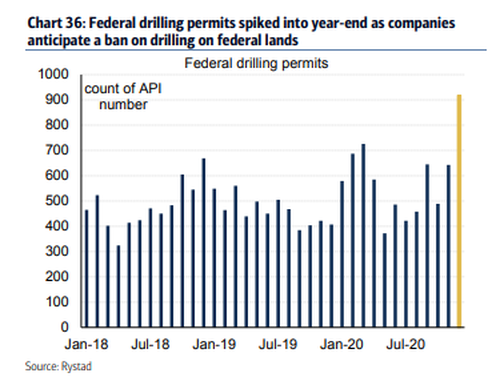

Yet while E&P companies sold off sharply on the news, one can argue that the decision wasn’t exactly a surprise for the drillers themselves, because as the following chart from BofA shows, federal drilling permits spiked into year-end as companies clearly anticipated a ban on drilling on federal lands.

But it’s not just speculation about what impact on drillers – and especially frackers will be – Biden’s intervention will have: an just as important question is what to expect on the price of oil as a result.

Well, overnight, Goldman’s commodity team said that a lack of urgency from the US government to lift Iranian sanctions and a push for larger fiscal spending support the constructive view on oil and gas prices; at the same time it estimated that a 2 trillion stimulus over 2021-2022 would increase US demand by 200k bpd and stated that delays in a full return of Iran production would support the bullish oil outlook. Goldman’s summary, which could say is obvious: “policies to support energy demand but restrict hydrocarbon production (or increase costs of drilling and financing) will prove inflationary in coming years given the still negligible share of transportation demand coming from EVs (and renewables).”

In short, just what Putin and the Crown Prince ordered.

Below we excerpt from Goldman’s note:

Initial orders by the Biden administration include restrictions on North American hydrocarbon leasing, drilling and pipelines. In turn, initial comments suggest no urgency in lifting sanctions with Iran. Combined with a push for greater fiscal spending – and hence higher energy demand – these initial actions reinforce our constructive view on oil and gas prices. As we have argued, policies to support energy demand but restrict hydrocarbon production (or increase costs of drilling and financing) will prove inflationary in coming years given the still negligible share of transportation demand coming from EVs (and renewables).

- The Interior Department imposed on Wednesday a 60-day moratorium on oil and gas leases and drilling permits on federal lands, minerals, and waters. This order is temporary and has no impact on near-term activity as producers had aggressively accumulated federal drilling permits. While temporary, this order nonetheless suggests that the new administration views its pledge to halt leasing on federal lands as a priority of its climate plan, with such a broader moratorium on federal leasing potentially scheduled for next week according to Bloomberg. As we argued ahead of the election, such actions point to both higher production and financing costs for shale producers in coming years as well as lower recoverable resources. The additional orders to impose a moratorium on leasing activity in Alaska’s Arctic National Wildlife Refuge and to revoke Keystone XL’s border permit point to a similar regulatory shift.

- On their own, these actions do not point to a faster tightening of the oil market. in 2021-22, as a ban on permitting would still leave a window of up to two years to drill from elevated outstanding permits. In fact, this would likely shift drilling activity away from private to federal land (for example from the Midland to the Delaware basin) for a couple years to minimize the loss of recoverable resources. While producers are focused on shareholder returns over production growth,investors may support more aggressive drilling to secure future cash flows, potentially creating a modest headwind to sharply higher oil prices in the next few years. The administration’s focus on fiscal spending and recent foreign policy comments are, however, likely to help tighten the oil market in 2021-22.

- The release of President Biden’s COVID-relief plan has led our economists to increase their assumption for additional fiscal measures from $750bn to $1.1tn. Larger boosts to disposable income and government spending will make this recovery energy intensive long before it hurts oil demand, in our view, especially as they come alongside those in China and the EU. On our estimates, a $2 trillion stimulus over 2021-22 would for example boost US demand by c. 200 kb/d. Such spending would further contribute to a weakening dollar which itself lends support to oil prices. A faster vaccination roll-out would in turn accelerate the rebound in jet fuel consumption, which still accounts for more than half of the remaining lost oil demand.

- Finally, the new administration’s focus on reaching bi-partisan policy support suggest a lessened incentive to quickly revisit the divisive Iran nuclear deal. While the US president has significant freedom to re-enter the JCPOA agreement (see Appendix),the confirmation hearing for the US Secretary of State and Treasury Secretary focused on the need for consultation with Congress and US allies, on Iran being non-compliant and on the goal of reaching a stronger and longer new deal. We view such statements as consistent with our assumption that the increase in Iran exports will remain moderate in 2021 (we assume 0.5 mb/d in 2H21) with in fact risks that our assumed full recovery in Iran production in 2Q22 proves optimistic. Delays in a full return of Iran production would reinforce our bullish oil outlook since we already forecast a tight 2022 crude market with low OPEC spare capacity.

- Stronger demand and a slower ramp-up in Iran production would create a larger call non shale production, which will face higher regulatory costs, leading to further increases in long-dated oil prices. The oil market experienced such an outcome in 2018, when the loss of Iran production and strong economic growth pushed oil prices sharply higher. As we argued at the time, the rally to $80/bbl Brent prices was necessary to bring high-cost Bakken barrels to the global market by rail. Notably, the potential halt to Dakota Access Pipeline flows could recreate such conditions incoming years (the pipeline may need a new Environmental Impact Study from the Army Corps of Engineers, which is led by a presidential appointee which could stay its operations).

*********

(TLB) published this article from ZeroHedge as compiled and written by Tyler Durden.

••••

••••

Stay tuned to …

••••

The Liberty Beacon Project is now expanding at a near exponential rate, and for this we are grateful and excited! But we must also be practical. For 7 years we have not asked for any donations, and have built this project with our own funds as we grew. We are now experiencing ever increasing growing pains due to the large number of websites and projects we represent. So we have just installed donation buttons on our websites and ask that you consider this when you visit them. Nothing is too small. We thank you for all your support and your considerations … (TLB)

••••

Comment Policy: As a privately owned web site, we reserve the right to remove comments that contain spam, advertising, vulgarity, threats of violence, racism, or personal/abusive attacks on other users. This also applies to trolling, the use of more than one alias, or just intentional mischief. Enforcement of this policy is at the discretion of this websites administrators. Repeat offenders may be blocked or permanently banned without prior warning.

••••

Disclaimer: TLB websites contain copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to our readers under the provisions of “fair use” in an effort to advance a better understanding of political, health, economic and social issues. The material on this site is distributed without profit to those who have expressed a prior interest in receiving it for research and educational purposes. If you wish to use copyrighted material for purposes other than “fair use” you must request permission from the copyright owner.

••••

Disclaimer: The information and opinions shared are for informational purposes only including, but not limited to, text, graphics, images and other material are not intended as medical advice or instruction. Nothing mentioned is intended to be a substitute for professional medical advice, diagnosis or treatment.

Leave a Reply