“Happy Days Are Here Again… But You Can’t Print Grain, Or Oil, Or Uranium”

By Benjamin Picton, senior strategist at Rabobank

![]()

US non-farm payrolls underwhelmed on Friday, and it is clear that inflation is now defeated. Well, not really. But you wouldn’t know it from the way the bond market reacted to the figures. The US 10-year treasury yield gave up 14bps after official figures showed that employment rose by *only* 187,000 in July. The market was looking for a gain of 200,000, so it was a slight miss for the month. The source of much of the optimism seems to be downward revisions for employment in June and May, but even with those revisions employment is still growing faster than the labor force. Consequently, the unemployment rate ticked lower to 3.5% and growth in average hourly earnings held at 4.4%. Conclusive?

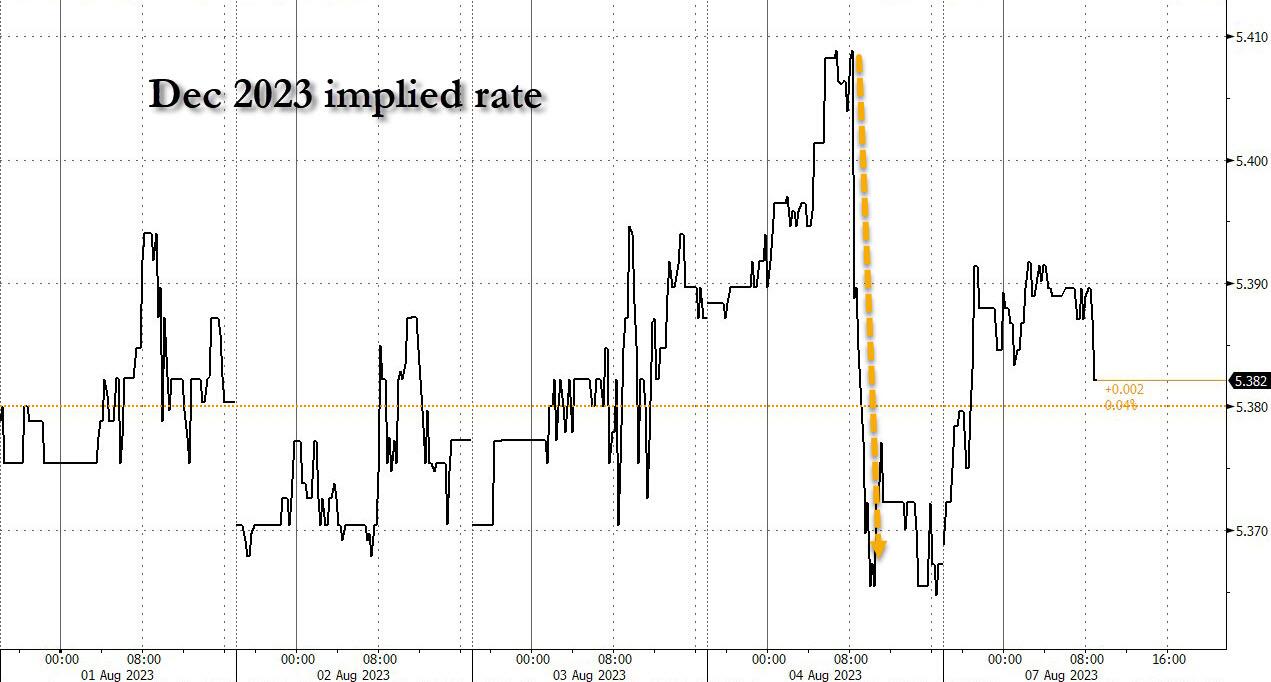

Bond market jubilation wasn’t completely contained to the long end. There wasn’t much movement in the implied probability of a further rate hike in the Fed Funds futures, but the implied rate as at December next year fell by about 10bps. The bond market seems to be suggesting that the jobs figures point to a faster economic slowdown and more active easing cycle from the Fed in an attempt to pilot the economy into a beautiful soft landing, rather than ending up as a dark smudge on the tarmac.

While the bond market went Pollyanna on Friday, equities read things differently. The S&P500 was off by more than half a percentage point and the NASDAQ down by more than a third of a percentage point (with tech stock valuations no doubt supported by falling bond yields). The Dow Jones has now fallen for three straight sessions after setting a new record for most consecutive up days between July 10th and 26th (13 in a row). “Sell in May and go away” appears to have been bad advice this year, but are we now at the beginning of an overdue correction in equity markets? A cursory check of the total assets on the Fed’s balance sheet show that we are now back below the levels reached in early March, before the collapse of SVB, Signature Bank and First Republic necessitated another one of those ‘mid-course corrections’ whereby balance sheet reduction was put into hard reverse.

Between July and September the US Treasury is expecting to cram more new issuance into the market than was previously suggested. Lower tax receipts, higher outlays and the effects of the debt ceiling negotiations earlier in the year on delaying new issuance seems to have created a bulge in the debt marketing pipeline. While the Treasury is mopping up cash, the Fed has also swung from being a net buyer of debt to a net seller, suggesting that securities will be more plentiful and cash more scarce. This, combined with the perception that we are nearing the end of the Fed hiking cycle is a likely driver for the bear steepening that we have seen since the end of June.

P/E ratios on the S&P500 are above 20x at the moment. So, as they say on Twitter: “whomst equity risk?” With valuations that high, and dividend yields running at a piddling 1.54%, it seems hard to get bulled-up on equity beta from here. That may be why we are seeing average 1-day price moves following earnings releases showing negative for every sector except materials and financials despite broadly strong bottom-line growth. So, is this as good as it gets for equities? Or does the prospect of an impending easing cycle from central banks present enough of a carrot to keep equities bid as a relative value play versus bonds?

Developments in commodity markets are even more interesting. My colleague Teeuwe Mevissen covered Belarussian incursions into Polish airspace and Russian rocket attacks on Ukrainian grain facilities close to the Romanian border last week. This morning we are seeing CBOT wheat futures up more than 11USc/bu following reports of a Ukrainian drone strikes on a Russian warship and oil tanker in the Black Sea over the weekend. The situation is developing into a tit-for-tat as Ukraine seeks to cripple Russia’s capacity to fund its war effort through commodity exports.

Understandably, the world’s gaze is fixed on the situation in Ukraine, but this isn’t the only flashpoint for commodities. Last Tuesday we wrote about the coup in Niger impacting upon the supply of uranium to the French nuclear industry. Niger supplies 25% of Europe’s uranium, and signs that the military junta is cosying up to Wagner Group potentially puts close to 60% of the world’s mined uranium under the influence of the Kremlin. Even more concerningly, Russia itself dominates the market for uranium enrichment, while the West has allowed its own capabilities in this area to wither on the vine via comforting delusions of the End of History. Clearly there are many risks here, with potentially severe implications for energy security and decarbonisation efforts.

The United States is alive to these risks, but has perhaps been too slow off the mark in addressing them and in convincing her allies to do the same The Associated Press reported over the weekend that the US is considering stationing military personnel on commercial ships traversing the Strait of Hormuz to deter Iranian seizures of tanker vessels. This would be an unprecedented move aimed at ensuring the integrity of 20% of the world’s oil trade, which flows through the region. Again, Western Europe has the most to lose here.

So, yields are down for the time being but you can’t print grain, or oil, or uranium, so risks of further supply shocks remain….

For the time being though, happy days are here again!

*********

(TLB) published this article By Benjamin Picton, senior strategist at Rabobank, as posted at ZeroHedge

Header featured image (edited) credit: Happy Days TV cast/org. post via ZH

Emphasis added by (TLB)

••••

••••

Stay tuned to …

••••

The Liberty Beacon Project is now expanding at a near exponential rate, and for this we are grateful and excited! But we must also be practical. For 7 years we have not asked for any donations, and have built this project with our own funds as we grew. We are now experiencing ever increasing growing pains due to the large number of websites and projects we represent. So we have just installed donation buttons on our websites and ask that you consider this when you visit them. Nothing is too small. We thank you for all your support and your considerations … (TLB)

••••

Comment Policy: As a privately owned web site, we reserve the right to remove comments that contain spam, advertising, vulgarity, threats of violence, racism, or personal/abusive attacks on other users. This also applies to trolling, the use of more than one alias, or just intentional mischief. Enforcement of this policy is at the discretion of this websites administrators. Repeat offenders may be blocked or permanently banned without prior warning.

••••

Disclaimer: TLB websites contain copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to our readers under the provisions of “fair use” in an effort to advance a better understanding of political, health, economic and social issues. The material on this site is distributed without profit to those who have expressed a prior interest in receiving it for research and educational purposes. If you wish to use copyrighted material for purposes other than “fair use” you must request permission from the copyright owner.

••••

Disclaimer: The information and opinions shared are for informational purposes only including, but not limited to, text, graphics, images and other material are not intended as medical advice or instruction. Nothing mentioned is intended to be a substitute for professional medical advice, diagnosis or treatment.

Leave a Reply