Jan Credit Growth Craters – Interest Rates Soar

Consumers Hit A Brick Wall

![]()

Last month we showed the latest confirmation that the US economy was sliding into a recession: according to the latest, January, Senior Loan Officer Opinion Survey held by the Fed, the economic situation in the US had gotten especially dire in the past few months as on one hand, banks have sharply tightened lending standards for commercial, mortgage and credit card loans, making credit – that beating heart that sustains the US economy – scarce…

… while on the other, demand for credit – a function of soaring interest rates – also collapsed.

But where is the evidence, the skeptics asked, and rightfully so: after all, the recent monthly consumer credit reports showed near record increases in both revolving (credit card) and non-revolving (student and auto loan) credit.

We didn’t have long to wait for Exhibit A that the US consumer appears to have finally hit a brick wall.

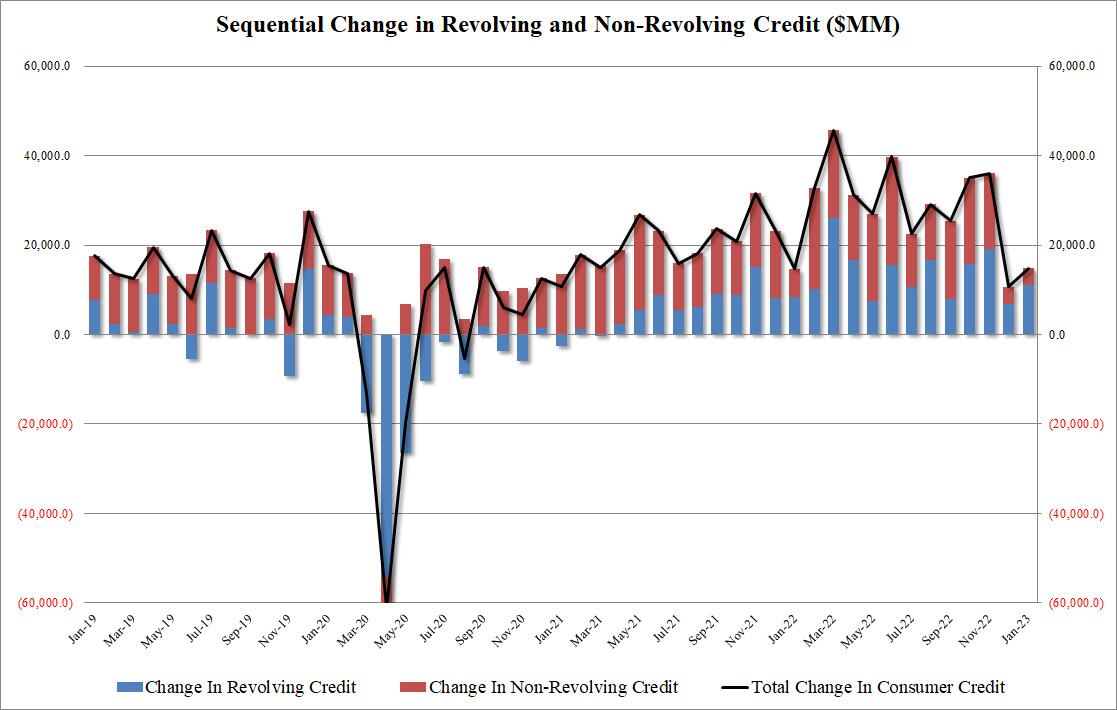

One month ago, the Fed’s December consumer credit report found that total US consumer credit increased by just $11.565Bn, which was not only a huge, 65% drop from November’s upward revised $33.1Bn print, but also a massive 50%+ miss relative to consensus expectations of $25BN, the biggest miss since August 2020!

Fast forward one month when consumer credit just stumbled for the second month in a row: in January, consumer credit rose just $14.8BN, a modest increase from last month’s downward revised $10.7BN, but a huge miss to the median consensus estimate of $25.4BN.

This was the second consecutive big miss in a row, similar in size to the collapse observed in March and April 2020.

What caused the sharp slowdown in consumer credit which has traditionally increased by anywhere between $20BN and $30BN, rain or shine? Well, there was a slowdown in revolving, or credit card debt, which increased $11.2BN in January, an improvement from the $6.9BN in December, if below the LTM average of $13.4BN.

But the real driver behind the shocking hit was non-revolving credit, which rose by just $3.6 BN, below last month’s already sharply depressed $3.8BN (downward revised from $4.4BN) and the $15.7BN LTM average.

For those asking if the surge in interest rates in Q3 and Q4 had anything to do with it, the answer is a resounding yes: as of Dec 2022, the average credit card rates according to the Fed, was 20.40%, the highest on record in the Fed’s database.

Bottom line is simple: while US savings (especially excess covid savings) were spent long ago and flatlined near record lows in recent months, it was all up to credit cards and other sources of (repurposed) credit – like pretending one’s student loans are actually going to, you know, studying when instead they were used to buy iPhones, TVs, booze and onlyfans subs – to drive consumers.

However, the recent surge in rates has meant that even the indomitable US addiction to credit is finally coming to an end, and the result is a sharp slowdown in credit-funded purchases, alongside an upward inflection in savings as US consumers are realizing the good old stimmy days are gone and more money has to be set side, and thus not spent.

And since the US consumer is 70% of US GDP, this may be the clearest sign yet that 2023 GDP is about to hit a similarly sized brick wall. Which is great news for the Fed: after all, a recession is precisely what Powell wanted… and is about to get it.

_________

RELATED

Why Student Loan Debt Relief Is A Worse Idea Than You Think

*********

(TLB) published this article from ZeroHedge as compiled and written by Tyler Durden

Header featured image (edited) credit: Consumer tapout graphic/org ZH post

Emphasis added by (TLB) editors

••••

••••

Stay tuned to …

••••

The Liberty Beacon Project is now expanding at a near exponential rate, and for this we are grateful and excited! But we must also be practical. For 7 years we have not asked for any donations, and have built this project with our own funds as we grew. We are now experiencing ever increasing growing pains due to the large number of websites and projects we represent. So we have just installed donation buttons on our websites and ask that you consider this when you visit them. Nothing is too small. We thank you for all your support and your considerations … (TLB)

••••

Comment Policy: As a privately owned web site, we reserve the right to remove comments that contain spam, advertising, vulgarity, threats of violence, racism, or personal/abusive attacks on other users. This also applies to trolling, the use of more than one alias, or just intentional mischief. Enforcement of this policy is at the discretion of this websites administrators. Repeat offenders may be blocked or permanently banned without prior warning.

••••

Disclaimer: TLB websites contain copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to our readers under the provisions of “fair use” in an effort to advance a better understanding of political, health, economic and social issues. The material on this site is distributed without profit to those who have expressed a prior interest in receiving it for research and educational purposes. If you wish to use copyrighted material for purposes other than “fair use” you must request permission from the copyright owner.

••••

Disclaimer: The information and opinions shared are for informational purposes only including, but not limited to, text, graphics, images and other material are not intended as medical advice or instruction. Nothing mentioned is intended to be a substitute for professional medical advice, diagnosis or treatment.

Leave a Reply