The “Safety” Dance

We all need some good things to reflect on when “safety” and “security” are top of mind. ~Peter Tchir

By Peter Tchir of Academy Securities

On Wednesday, November 8th, Academy Asset Management (an affiliate of Academy Securities) celebrated the VETZ Veteran Impact ETF and Veterans Day at the New York Stock Exchange by ringing the closing bell. Safety was a big topic of conversation last week, and was highlighted during the geopolitical roundtable that Academy held at the NYSE. Issues covered included:

- Geopolitical and physical safety

- Investment safety

- Cyber security (or safety to fit within our theme)

- “Safe” assets

- Technological, economic, and trade “safety”

It doesn’t hurt that bringing up “The Safety Dance” brings back some good memories of a road trip to Montreal where we got to see Bootsauce live (a local up-and-upcoming band at the time). We all need some good things to reflect on when “safety” and “security” are top of mind.

It was nice that markets cooperated with the Bottom Line from last weekend’s What a Fire (some “consolidation” with a bias towards owning the “everything rally”).

We also got to discuss a variety of subjects (including “safety”) on Bloomberg TV on Wednesday (starts at around the 1:42:45 mark). Apparently, based on a lot of feedback, it was an interesting interview and worth watching. That feedback is at least partially supported by the fact that Bloomberg made a quick clip out of the Pain Trade portion of the interview and they used our line from the piece titled “Analysts Who Cried Recession” in the headline of a written report. Bloomberg also aired a replay of the energy discussion we had.

However, let’s get back to the issue of “safety.”

Geopolitical and Physical Safety

The battles between Israel and Hamas have intensified. As our Geopolitical Intelligence Group (“GIG”) has repeated over and over, it will be very difficult for Israel to eradicate Hamas as a threat. The complex tunnel network makes the urban fighting even more difficult than what the U.S. experienced in Fallujah. Setting up operations and command & control centers in and around civilian facilities (like schools and hospitals, which is prohibited by the Geneva Convention) makes the fighting more challenging.

On the “bright” side of things (to the extent that there is a bright side), so far there has been no escalation by other groups or countries in the region. That threat does exist, and will remain high while the fighting continues. This is a very tricky situation, but it has (so far) not escalated to the point of being a major global economic issue. However, I am hearing chatter about supply chain issues. The supply chain issues are centered around goods produced by Israel. There is also concern around the ability to ship things through the region (e.g. the Suez Canal) because the risk of escalation or even “accidents” is greatly increased.

Ukraine’s “counteroffensive” is all but over, and it seems like Russia may be turning the tide. The likelihood of the “stalemate” continuing seems high (though presumably, the Russians will attempt another winter offensive once the ground freezes). Support for weapons deliveries is now far from universal. However, while the quality and types of weapons being delivered are superior to what was delivered early in the war, many members of the GIG question whether it is enough to allow Ukraine to push Russian forces back across their border. Nothing good is happening in the war which, paradoxically, may be a good thing as it could push both sides to the table (though that is not likely until the spring). It is still unclear to me if this would result in much of an immediate impact to the global economy or even the inflationary pressures in Europe (Ride of the Valkyries).

“Safety” in Markets

As stocks seemed to defy gravity (or at least higher bond yields) on Friday to finish the day and the week up (1.3% to 2.4%, depending on the index you track), many are looking at “hedges.” That is in the “normal” realm of discussion topics. What is abnormal is this background buzz about whether Treasuries are “safe” assets.

The 10-year auction did well, but the 30-year auction struggled. That had absolutely nothing to do with the Fed. Yes, Powell spoke hawkish, but what else was he going to do or say? It has everything to do with:

- Higher inflation expectations. The concepts of geopolitical inflation, ESG inflation, and supply chain inflation are now widely held views. We continue to expect 3% to 5% inflation over the next 3 to 5 years from these various forces. However, we don’t think that the Fed will react aggressively to persistent inflation near 3%, precisely because of where it’s coming from. It would be good to see better messaging out of D.C. regarding why this sort of inflation (which goes hand in hand with creating a safer and more secure economy) is not only necessary, but good for us longer-term!

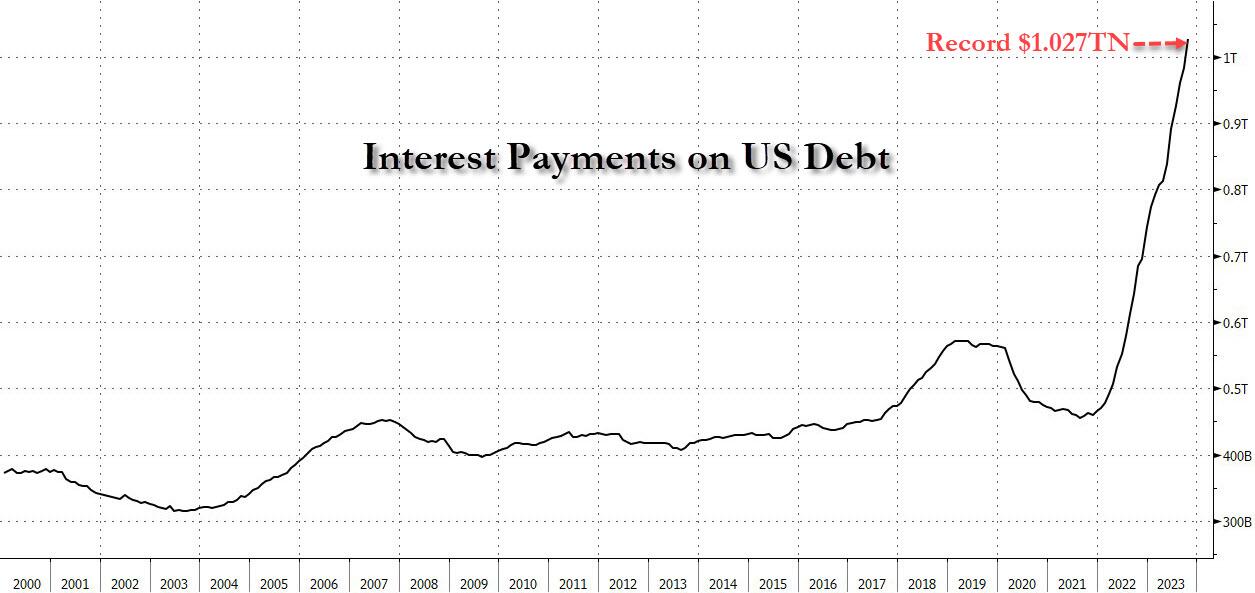

- Lack of control, discipline, and responsibility out of D.C. We discussed this in U.S. Credit on the back of some actions by the NRSROs (often referred to as rating agencies). Now, we are all watching the nation’s cost of borrowing rise rapidly as the combination of rising yields and more total debt becomes problematic. Some are using words other than “problematic” to describe the situation, but that is premature. Yes, we are on a bad trajectory, but both supply and the average coupon paid take time to reset significantly higher and too much is already priced in.

Treasuries are still “safe,” but in no way as “safe” as they were a year or two ago. Why would we even bother discussing the difference between “safe” and “still safe, but not as safe as before?” That is probably a good question, but I also wanted to point out that certain mathematicians have varying degrees of “infinite.” How can something that is infinite be bigger or smaller than something else that is infinite? Well, it can be, and I think that logic (although it hurts my head) is why it is appropriate to think about what is “safe.”

- I’m leaning towards being overweight floating rate assets. SOFR (for all intents and purposes) is set by the government/Fed. Sure it can spike for a day or two, but there are tools and policy support steps in place to keep it stable. The same cannot be said for longer-dated bonds. Longer-dated bonds, especially in this algo driven “faux” liquidity (Voldemort) environment, are susceptible to large moves. The risk of stops being triggered is real. Bond investors typically lose far more money from forced selling than they do from defaults. I think that being overweight floating debt (or short-term debt) could put you in a position to capture some “weird” days in bonds, where we get a large move in bond yields (3 or more standard deviations).

- Corporates (and Munis) versus government debt. Municipalities typically must operate with a balanced budget. In addition, corporations have governance. I really like the front end (5-years and in, with some floaters) of high-quality IG (A or better, I wanted to say BBB or better, but figured that I’d get too much push back) as spreads will do well as some choose corporates over government debt.

- Crypto. There, I said it! I’m not even sure that I really believe it, though it is coming up more often in discussions about “what is safe.” Clearly Bitcoin has surged recently and is back above $37,000. Other parts of the market have also done well. Certainly, hopes of a “spot” ETF have fueled those gains. Geopolitical unrest across the globe is likely helping as well, but I suspect that part of this rise is driven by investors looking for something “safe.” I’m not there yet (in terms of thinking that crypto is “safe”), but clearly others are and at least from a trading perspective, this theme could have legs as others think about what is “safe” or not.

- Stocks. In a world where we don’t “trust” the “safe” asset, maybe something that tends to benefit from government spending is “safer.” The one flaw here is that the debt that is increasing due to higher borrowing costs only really helps the savers, so I’m not sure how well that translates into corporate earnings or multiples that investors will pay.

Applying degrees of safety to government debt seems awkward, but we are there and not turning back any time soon.

Cyber Safety

We will be publishing some new “X Reports” (cyber, AI, and space focused) in the coming weeks, but two things really stuck out at the cyber/AI panel from Wednesday.

- Quantum computing. The potential obsolescence of existing encryption.

- How dangerous is the cyber world. Somehow the conversation on Wednesday turned to “number of attacks.” While some of the specific numbers are classified, the panelists seemed comfortable trying to point out that however high “we” (the audience) thought the numbers were, the real number was significantly higher. One example that was brought up, if I understood correctly, is that the NSA has a list of known malicious websites to which it helps block inadvertent access. This list is apparently in the billions! I started thinking about various letter and number combinations, and a billion seems like a lot. To put this in perspective, 1 million seconds is a bit less than 12 days. A billion seconds is over 31 years!

Very little about the cyber panel was comforting. In addition, this week a ransomware attack on a foreign financial institution caused some disruption in the U.S. Treasury market. However, the fact that companies and countries are acutely aware of the risks (and are working to stop them) is good. Also, we don’t hear much about the “successes” because that is the nature of cyber “warfare.”

Economic Safety

One thing that I could see happening is that the U.S. could reach some sort of “accord” with China in the coming weeks or months.

With so many “hot spots” across the globe, we could look to reduce tensions with China. Maybe we could back off on tariffs? We could also make some changes to what technology is prohibited from being traded.

I suspect that any such deal would cause us some longer-term problems as it would considerably help the “Made by China” story (which is gaining traction) and increase the risk of China gaining access to technology that we are trying to prevent them from accessing. Of note, the latest phones in China use chips that are thinner than the U.S. expected them to have at this point.

In the near-term, this kind of news would likely spark a major rally in risk assets.

Again, it seems convoluted that something that I don’t like long-term would help in the short-term. However, it does seem like the U.S. currently holds the “weaker hand” in trade negotiations with China (despite the obvious evidence of their economy slowing).

Bottom Line

Add some equity hedges and favor the “everything rally.” If nothing else, let’s not forget that:

“We can dance if we want to

We can leave your friends behind

Because your friends don’t dance

And if they don’t dance

Well, they’re no friends of mine.”

I write this knowing that I am a horrible dancer but wanted to end on a positive note because while we need to worry about “safety,” we also need to enjoy life!

_________

RELATED

The Fed Has No Plan, And Is Just Hoping For The Best

Treasury Auctions Explained For People With Short Attention Spans

Hartnett: Selling Panic Flips To Year-End Greed

*********

(TLB) published this article by Peter Tchir of Academy Securities as posted on ZeroHedge

Header featured image (edited) credit: Bootsauce/Safety Dance/YouTube grab

Emphasis added by (TLB)

••••

••••

Stay tuned to …

••••

The Liberty Beacon Project is now expanding at a near exponential rate, and for this we are grateful and excited! But we must also be practical. For 7 years we have not asked for any donations, and have built this project with our own funds as we grew. We are now experiencing ever increasing growing pains due to the large number of websites and projects we represent. So we have just installed donation buttons on our websites and ask that you consider this when you visit them. Nothing is too small. We thank you for all your support and your considerations … (TLB)

••••

Comment Policy: As a privately owned web site, we reserve the right to remove comments that contain spam, advertising, vulgarity, threats of violence, racism, or personal/abusive attacks on other users. This also applies to trolling, the use of more than one alias, or just intentional mischief. Enforcement of this policy is at the discretion of this websites administrators. Repeat offenders may be blocked or permanently banned without prior warning.

••••

Disclaimer: TLB websites contain copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to our readers under the provisions of “fair use” in an effort to advance a better understanding of political, health, economic and social issues. The material on this site is distributed without profit to those who have expressed a prior interest in receiving it for research and educational purposes. If you wish to use copyrighted material for purposes other than “fair use” you must request permission from the copyright owner.

••••

Disclaimer: The information and opinions shared are for informational purposes only including, but not limited to, text, graphics, images and other material are not intended as medical advice or instruction. Nothing mentioned is intended to be a substitute for professional medical advice, diagnosis or treatment.

Leave a Reply