Bank-Stress Is Wake-Up Call For Goldilocks

Elevated rates are cumulatively inflicting mounting damage across the economy

By Simon White – Bloomberg macro strategist

Banking sector problems are a prescient reminder that elevated rates are cumulatively inflicting mounting damage across the economy. Ironically, that ultimately means yields are heading higher.

The probability of deeper and perhaps sooner Federal Reserve rate-cuts and an earlier end to quantitative tightening has – even following Wednesday’s FOMC statement – risen at the margin after New York Community Bancorp’s dividend was cut and its equity fell by over a third. This will stoke already-burgeoning inflation pressures, ultimately leaving the US household sector as the buyer of last resort for Treasuries — and it will extract a much higher yield to do so.

Colonel Jessup in A Few Good Men complained that people couldn’t handle the truth. Well, neither can the heavily indebted US economy handle rates at 5.5%. NYCB may be a smaller bank saddled with commercial real estate losses and therefore prime facie facing different problems than Silicon Valley Bank last year, but the root cause is the same: elevated interest rates and too much duration.

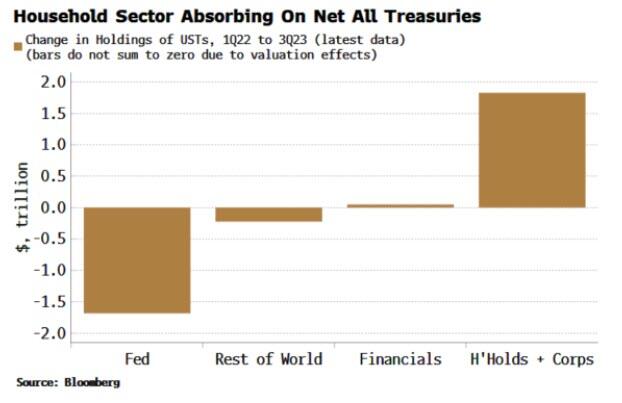

Instead, between the first quarter of 2022 — when the Fed started hiking rates — until the latest data from the third quarter of last year, the household and corporate sector has on net absorbed all of the over $1.5 trillion Treasuries that had hitherto been accommodated on the Fed’s balance sheet.

Why have financials not jumped at the chance to buy government debt? Wariness of massive supply is the obvious answer. But it is more nuanced than that. And in explaining this, we can see an actual mechanism of how higher inflation leads to higher yields.

The financial industry has grown rich and complacent on 60/40 portfolios – 60% equities, 40% bonds – or variations on this theme such as risk parity. That worked well in a regime of low-and-stable inflation as stocks and bonds tended to move oppositely to one another, making the second an effective hedge for the first.

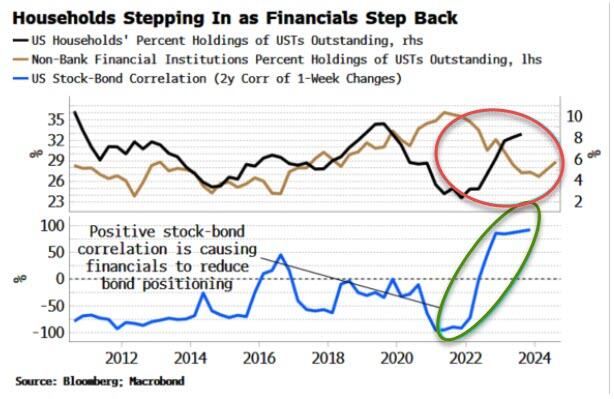

But in an elevated-inflation regime, a growth shock can be accompanied by an inflation shock, and stocks and bonds start to co-move more together. That means bonds no longer improve risk-adjusted returns in multi-asset portfolios, nor do they act as a recession hedge.

And in fact we find that the US non-bank financial sector – mutual funds, pension funds, hedge funds, etc – has on net been reducing its exposure to Treasuries as a percentage of the total outstanding as the stock-bond correlation has risen and moved into positive territory.

What’s more, who’s picked up the slack? The household sector, whose ownership of USTs rose from 2.4% to 8.3% of total Treasury debt from 1Q22 to 3Q23, while the non-bank financial sector’s fell from 34.7% to 27.3%.

Despite what plenty of backward-looking analysis says, inflation is not going anywhere, rather it is poised to re-accelerate this year. That means the stock-bond ratio is set to remain positive, massively challenging the shibboleth of 60/40 investing and making bonds a lot less desirable for anyone who doesn’t have liabilities they need to match (such holders currently account for a significant $6 trillion of UST holdings).

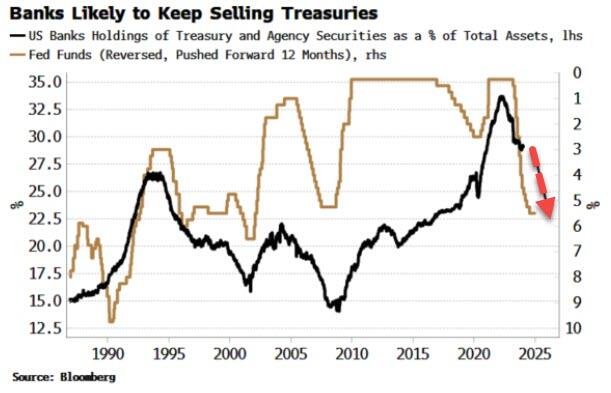

But it’s also from banks that the household sector has been absorbing Treasuries. They are more reactive than other holders of USTs, and they are typically quick to reduce their duration exposure when the Fed is raising rates.

They have reduced their UST and MBS holdings to just under 30% of assets, but that’s still historically high, and they have typically decreased their duration by more in previous rate-hiking cycles. (One caveat here is ongoing discussions about new US bank-capital requirements, which could eventually require them to hold more Treasuries, but this is not going to happen soon.)

There are therefore no imminent signs that banks and non-banks are about to backstop Treasury demand. The same goes for overseas buyers. There are many well-telegraphed reasons for foreign actors desiring to hold less US debt, such as America’s weaponization of its financial system, making return of capital no longer a sure-fire bet if you’re considered a wayward state.

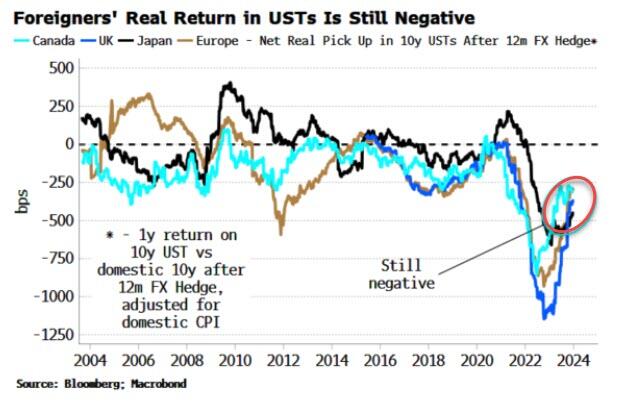

But for more mundane reasons – real interest-rate differentials – overseas buyers have just not been that into owning more Treasuries lately. The largest recent buyers are developed-market based – Canada, the UK, Japan, Europe, etc.

If we compare the net yield pick-up of what investors from these countries would earn by buying a 10y UST and hedging the FX versus their domestic government bonds, it has risen in recent months, and at the margin may be attractive, say for e.g. Germany, with a positive pick-up between bunds and Treasuries.

But inflation matters now. Adjusting the pick-ups for domestic price growth to get them in real terms, they remain significantly negative, making it unlikely we should soon expect foreign buyers of Treasuries to rush into absorbing much new issuance.

Here’s the rub. If the household sector is on the hook, it doesn’t have as anodyne a view of inflation as the market. As with the dictum that it’s impossible to get someone to understand something whose job depends on not understanding it, the market is expecting a return to 2% inflation as it does not know how to function in any other way.

Households aren’t buying it though. The sector’s expectations of long-term price growth are notably higher than their market counterparts, such as forward inflation swaps. As the chart below shows, household inflation expectations have been persistently higher than swaps since the mid-2010s.

That may not have mattered much before, but if households are now the marginal buyer of US Treasuries, then they also set the price. They’re unlikely to want them until longer-term yields are about 50-75 basis points higher, or more if inflation sees a resurgence.

Yields are lower in the wake of NYCB’s troubles: not only does that make them even less attractive to households, it’s a manifestation of deeper Fed cuts that will ultimately reignite inflation and pave the way for a secular rise in longer-term yields.

The buyer is happy to beware if the buyer also gets a margin of safety.

________

RELATED

The US Is Living On Borrowed Time

DoubleLine’s Gundlach Doubles Down On Recession As The Other “Big Short” Is Now “Blissfully Long”

CRE Crisis Goes Global: Shares Of Japan’s Aozora Bank Implode On Massive US CRE Exposure

*********

(TLB) published this article by Simon White as posted at Bloomberg and ZeroHedge

Header featured image (edited) credit: You Can’t Handle…/org. Bloomberg post

Emphasis added by (TLB)

••••

••••

Stay tuned to …

••••

The Liberty Beacon Project is now expanding at a near exponential rate, and for this we are grateful and excited! But we must also be practical. For 7 years we have not asked for any donations, and have built this project with our own funds as we grew. We are now experiencing ever increasing growing pains due to the large number of websites and projects we represent. So we have just installed donation buttons on our websites and ask that you consider this when you visit them. Nothing is too small. We thank you for all your support and your considerations … (TLB)

••••

Comment Policy: As a privately owned web site, we reserve the right to remove comments that contain spam, advertising, vulgarity, threats of violence, racism, or personal/abusive attacks on other users. This also applies to trolling, the use of more than one alias, or just intentional mischief. Enforcement of this policy is at the discretion of this websites administrators. Repeat offenders may be blocked or permanently banned without prior warning.

••••

Disclaimer: TLB websites contain copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to our readers under the provisions of “fair use” in an effort to advance a better understanding of political, health, economic and social issues. The material on this site is distributed without profit to those who have expressed a prior interest in receiving it for research and educational purposes. If you wish to use copyrighted material for purposes other than “fair use” you must request permission from the copyright owner.

••••

Disclaimer: The information and opinions shared are for informational purposes only including, but not limited to, text, graphics, images and other material are not intended as medical advice or instruction. Nothing mentioned is intended to be a substitute for professional medical advice, diagnosis or treatment.

Leave a Reply