There Goes The Second Tech Bubble: 2019 Set To Be The Worst Year For IPOs In History

Much has been said about the devastating impact that WeWork’s catastrophic failed IPO has had on capital market sentiment, and one needs look no further than the performance of the latest dismal IPO attempt, that of glorified stationary bike with an iPad superglued to it, Peloton, also known as WeBike, to see how profound the investor carnage has been.

Yet while we discussed extensively the post-WeWork pain spreading across the IPO world – as markets are finally “emerging from a psychotic break with reality” in Scott Galloway’s inimitable words – in “Buyer Beware: Peloton IPO Crash Tells Us The Global IPO Market Is Going Bust“, Goldman has what may be the definitive verdict on just how bad for IPOs 2019 is shaping up to be.

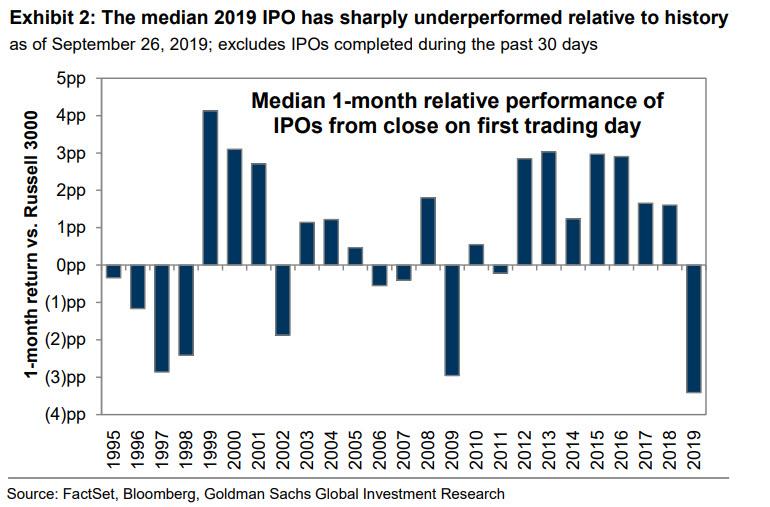

As the following chart shows from Goldman’s David Kostin, the median IPO in 2019 is now drastically underperforming the Russell 3000 relative to history; in fact, the roughly 3% underperformance is the worst on record, and surpasses the negative returns observed at the peak of the financial crisis in 2009 and in the aftermath of the bursting of the first dot com bubble.

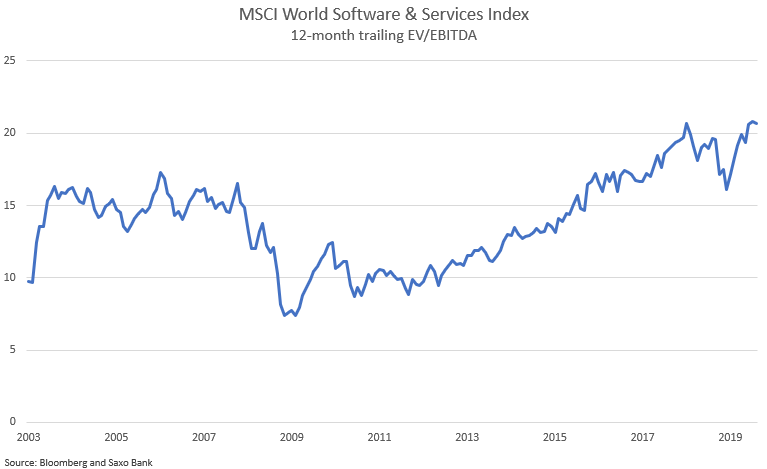

Tangentially related to this, Saxo Bank’s Peter Garnry writes that the second largest US industry group, Software & Services, is now valued in the 99% percentile on EV/EBITDA; “not a good recipe for future returns.” As Garnry notes, “we often just talk about valuations as something abstract but one has to realize that EV/EBITDA just above 20x means an implied return expectation by investors of around 4.8%”, which prompts him to ask “is that really a fair hurdle rate to expect for your capital given where we are in the business cycle? Our view is that valuations on software companies have reached unsustainable levels given the outlook and the risk-reward ratio is just terrible.”

So is the party finally over, and did the messianic, and now former, WeWork CEO, Adam Neumann, burst the biggest asset bubble of all time? For now the answer is unclear, but as Morgan Stanley’s Michael Wilson wrote on Sunday, the recent failure of We Company to go public is reminiscent of past corporate events marking important tops in powerful secular trends:

- United Airlines’ failed LBO in October 1989, which effectively ended the high yield/LBO craze of the 1980s.

- The AOL/TWX merger in January 2000, bringing the Dotcom bubble to a close.

- JPM’s take-under of Bear Stearns in March 2008, which signaled the end of the financial excesses of the 2000s.

“So if this is THE event, what are we ending”, Wilson asked, and answered:

In my view, the days of endless capital for unprofitable businesses. It was one heck of a run, but paying extraordinary valuations for anything is a bad idea, particularly for businesses that may never generate a positive stream of cash flows. If you ask me, that’s just common sense and it’s a good thing if the markets go back to a more disciplined mindset. The problem is that some stocks in the public markets still need to fall back to earth, and they reside in the secular growth category.

He’s right, of course, but with the fate of the US presidency and the Fed now both dependent on the market not falling, expect one hell of a fight before it all follows WeWork into collapsing into the dust of post-psychotic reality.

*********

(TLB) published this article from ZeroHedge with our appreciation to Tyler for the coverage.

••••

••••

••••

••••

Stay tuned to …

••••

The Liberty Beacon Project is now expanding at a near exponential rate, and for this we are grateful and excited! But we must also be practical. For 7 years we have not asked for any donations, and have built this project with our own funds as we grew. We are now experiencing ever increasing growing pains due to the large number of websites and projects we represent. So we have just installed donation buttons on our websites and ask that you consider this when you visit them. Nothing is too small. We thank you for all your support and your considerations … (TLB)

••••

Comment Policy: As a privately owned web site, we reserve the right to remove comments that contain spam, advertising, vulgarity, threats of violence, racism, or personal/abusive attacks on other users. This also applies to trolling, the use of more than one alias, or just intentional mischief. Enforcement of this policy is at the discretion of this websites administrators. Repeat offenders may be blocked or permanently banned without prior warning.

••••

Disclaimer: TLB websites contain copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to our readers under the provisions of “fair use” in an effort to advance a better understanding of political, health, economic and social issues. The material on this site is distributed without profit to those who have expressed a prior interest in receiving it for research and educational purposes. If you wish to use copyrighted material for purposes other than “fair use” you must request permission from the copyright owner.

••••

Disclaimer: The information and opinions shared are for informational purposes only including, but not limited to, text, graphics, images and other material are not intended as medical advice or instruction. Nothing mentioned is intended to be a substitute for professional medical advice, diagnosis or treatment.

Leave a Reply